How Credit Scores Affect Home Equity Loan Rates in 2025, Ontario Homeowner Guide

May 26, 2025

Updated July 2025

The home equity loans are mostly used for improvements that raise the value of the property, like adding a room or renovating.

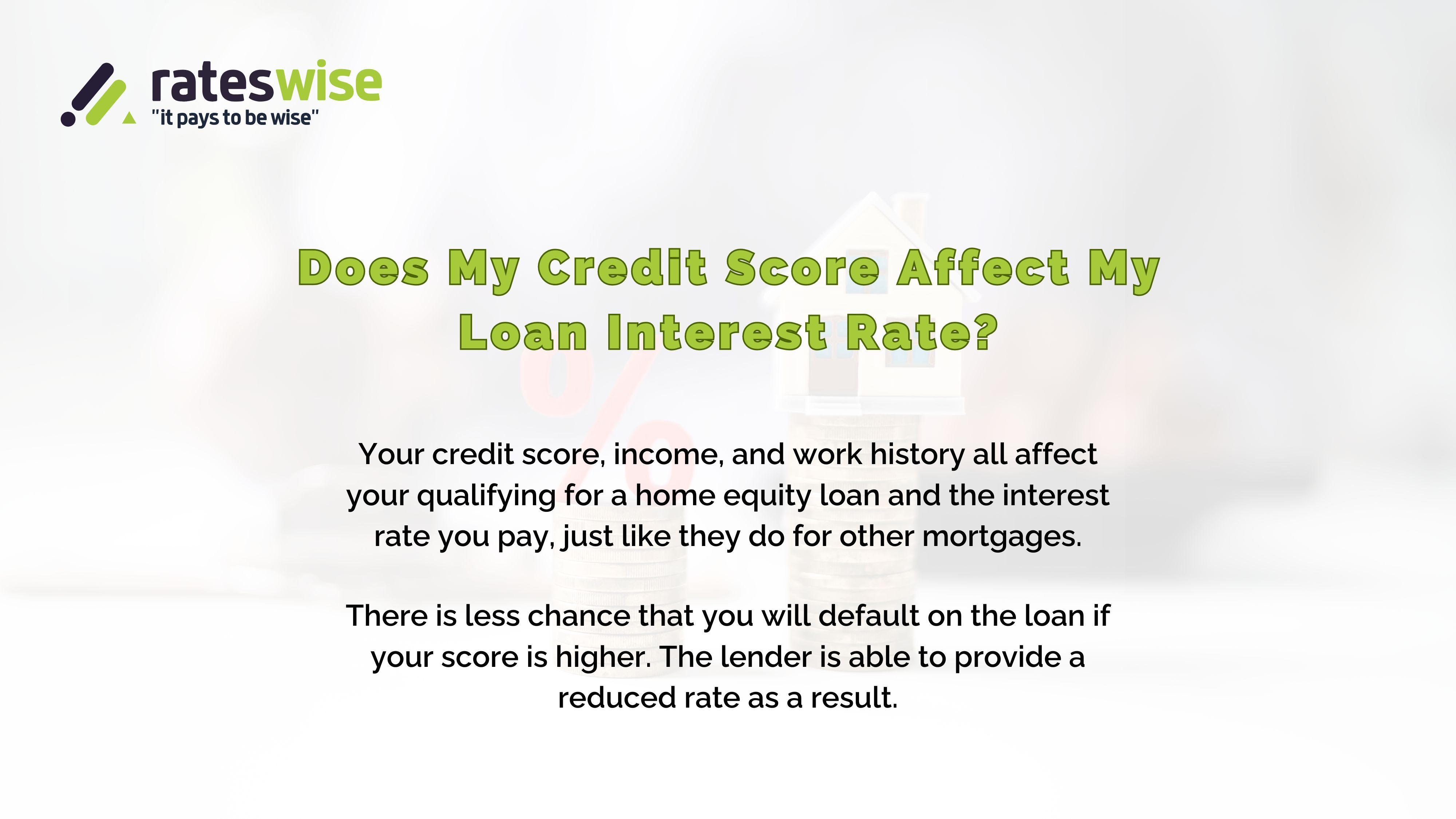

When you want to take out a home equity loan as a homeowner, your credit score is a crucial factor that evaluates your eligibility.

Even if you are already eligible for a mortgage, you still need to prove your creditworthiness. Your credit score determines your approval and denial, and also describes the interest rate you’ll get.

You can eventually save money and get better loan terms if you understand this relationship and how credit scores and home equity loans work.

Let's get started and learn about credit scores.

Understanding of the Credit Score:

Typically, a credit score in Canada falls between 300 and 900. As your score rises, so does your eligibility for a loan.

Here are some of the factors that go into calculating it:

Payment history: Missed or late payments might lower your score, but on-time payments raise your credit score.

Credit card usage: The proportion between the limits on your credit cards and their balances. The less you use, the better.

Duration of the credit history: Your score may increase if you have a lengthy credit history.

The Impact of Credit Scores on Home Equity Loan Interest Rates

Lenders evaluate your credit score to determine how risky it is to give you money.

- A higher score determines less risk and frequently leads to:

- Reduced Interest Rates

- Higher loan amounts

- Improved loan terms

- A low credit score can lead to:

- Higher interest rates

- Lower amounts to borrow

- Not flexible terms

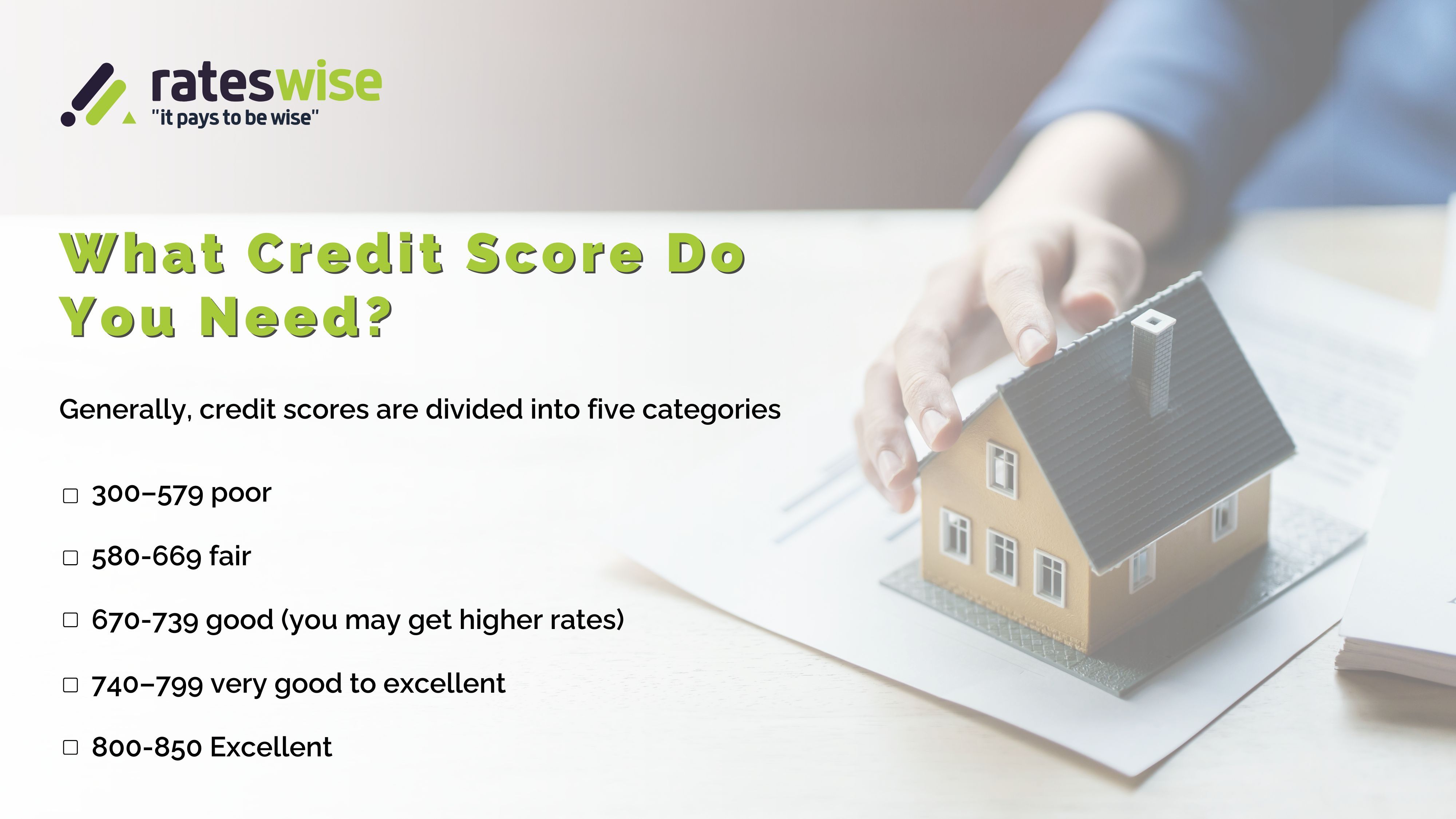

Credit Score Requirements in Canada

These requirements may vary from lender to lender, but mostly, this is the general guide here:

A credit score of 700 is considered excellent and may be considered favorable; you can get the desired rates/amount.

A 620-699 credit score is considered fair; you may get higher rates.

Less than 620 is considered poor; the conditions might not be favorable, and maybe you won’t even get approved.

It's critical to understand how credit scores affect your loan possibilities. If you have a worse credit score, some lenders might still approve you, but be careful to understand the potential risks.

July 2025 Canadian Rate Update

- The Bank of Canada held its overnight rate at 2.75% on June 4, 2025, keeping the prime rate steady at 4.95%.

- Because of this, home equity loan rates stay the same, usually ranging from 5.25% to 6.1%, depending on the lender and credit.

- With a potential cut later this year if prices are going up slowly, analysts anticipate the Bank to remain on hold until its next meeting on July 30.

How to Improve Your Credit Score

- Analyze your credit reports. Why are they declining?

- Your credit score is largely influenced by your payment history. Pay off your credit cards, auto loans, and other bills as a result your credit score will rise.

- The larger the difference between your debt and credit limit, the better. Credit usage should be less than 30%.

Wrapping Up

Your credit score impacts whether you’re eligible to get a home equity loan or not, and what would be the interest rates.

So it is important to learn the relationship between credit score and home equity loan rates, and how they impact.

If you have a good credit profile, you may get a home equity loan at a favorable rate. Be sure to raise your credit score before applying for a home equity loan.

Want a better rate? Get your free home equity loan quote with Rateswise now!

FAQs

What credit score do I need for a home equity loan in Canada?

Fair rates may begin at 620–699, while strong lenders usually demand 700+. Rates below 620 may restrict options.

Can I get a lower interest rate if my credit score is higher?

Yes, you can save hundreds of dollars annually by lowering rates by tenths of a percent for every 20 to 30 points you raise your score.

How fast can I improve my credit score?

Use less than 30% of your credit, pay your bills on time, and hold onto your old cards. In two to three months, your credit score can increase by 30 to 50 points.

Will checking my credit hurt my score?

While too many hard pulls from various lenders may have an impact on your credit score, Rateswise uses soft enquiries, which don't.

Disclaimer: This blog is intended for informational purposes only. Always consult with the lender or financial advisor for recent rates and updates.

About the Author

Written by Rateswise Team

Rateswise is a team of mortgage content strategists and professionals who specialize in home equity, refinancing, and Canadian lending insights. We are situated in Ontario, and we give Canadians clear, useful advice to help them make better mortgage decisions.

Related Articles