Refinance Mortgage Loan Guide for Ontario Homeowners

September 30, 2025

Updated: September 2025

Intro

Refinancing your mortgage in Ontario can help you save money or pay off your house more quickly if you own one. With a mortgage refinance, you get a new loan in place of your existing one. This guide describes the costs, procedures, and best practices for refinancing mortgage loans in 2025. In the summer of 2025, posted 5-year conventional rates were approximately 6.09%, while the Bank of Canada policy rate, which has been stable since July, is 2.75%. When looking for rates, that counts.

What is a refinance mortgage loan?

Your previous mortgage is replaced with a new one through a refinance loan. Either the term duration, the interest rate, or both may be altered. It is referred to as a rate-and-term refinance if you just alter the rate and term. A cash-out refinance is a separate product that occurs when you take out cash while borrowing more than you owe.

Common reasons that Ontario homeowners refinance

- Get a lower interest rate.

- Switch between variable and fixed, or the other way around.

- Reduce the length of your mortgage to repay the loan faster.

- Combine high-interest debt into your mortgage.

- Use equity for major expenses or improvements.

How a mortgage refinance works — simple steps

- Check for penalties on your existing mortgage.

- Calculate your home equity by subtracting your mortgage from its value.

- To find the best deals, compare brokers and lenders.

- Apply and provide documentation, including proof of income.

- To verify the worth of a residence, an appraisal could be necessary.

- Pay down the previous mortgage and close the new one.

Tip: You risk losing all of your savings if your prepayment penalty is high. Do the break-even calculation every time.

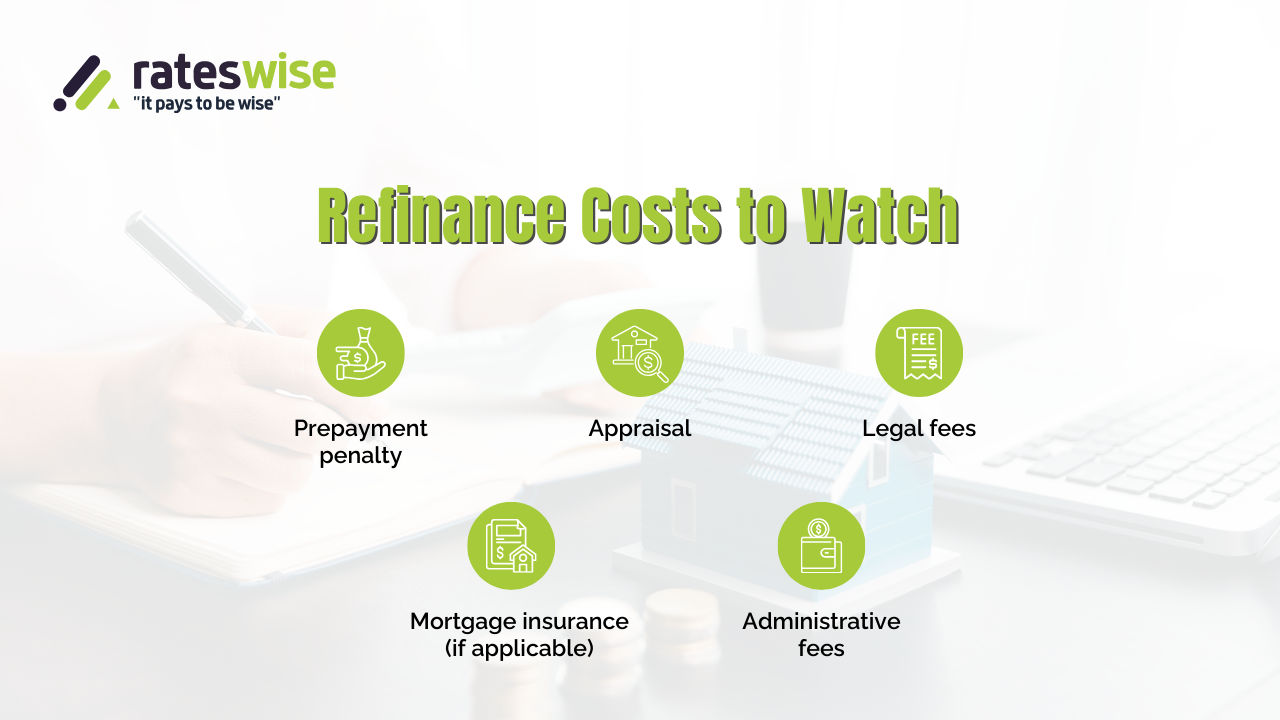

Costs and risks to be aware of

- For the potential large prepayment penalty.

- Appraisal and legal fees, which typically range from $800 to $2,000.

- Although longer amortization can result in affordable payments, the overall amount of interest paid will rise.

- Missing payments could result in foreclosure because your house is collateral

Is now a good time to refinance in Ontario?

Perhaps. Since July 2025, the Bank of Canada has maintained its policy rate at 2.75%. That's what lenders use to determine posted and prime rates. Although many lenders provide lower negotiated rates, the advertised 5-year conventional rate in mid-2025 was approximately 6.09%. Refinancing may make sense if you can get a rate that is far lower than your existing one. To ensure that the savings are real, it is crucial to verify fees and penalties.

How to get the best refinance mortgage in Ontario?

- Before you apply, raise your credit score.

- Investigate many lenders, including brokers, banks, and credit unions.

- Inquire about discounted fees (certain lenders do not charge for legal or appraisal expenses).

- Apply at the right time because lenders occasionally change their rates close to the end of the month or quarter.

- If you want access to wholesale rates, get a broker. Rateswise can help you get in touch.

Case example — how it worked for a family in Oakville

A couple had twelve years left on their 4.9% mortgage. The value of their house had increased. They reduced the term to ten years and refinanced at a rate of 4.0%. They saved over $18,000 in interest during the new term, but their monthly payment decreased significantly. They still won even after paying a $1,800 penalty and $1,200 in closing expenses.

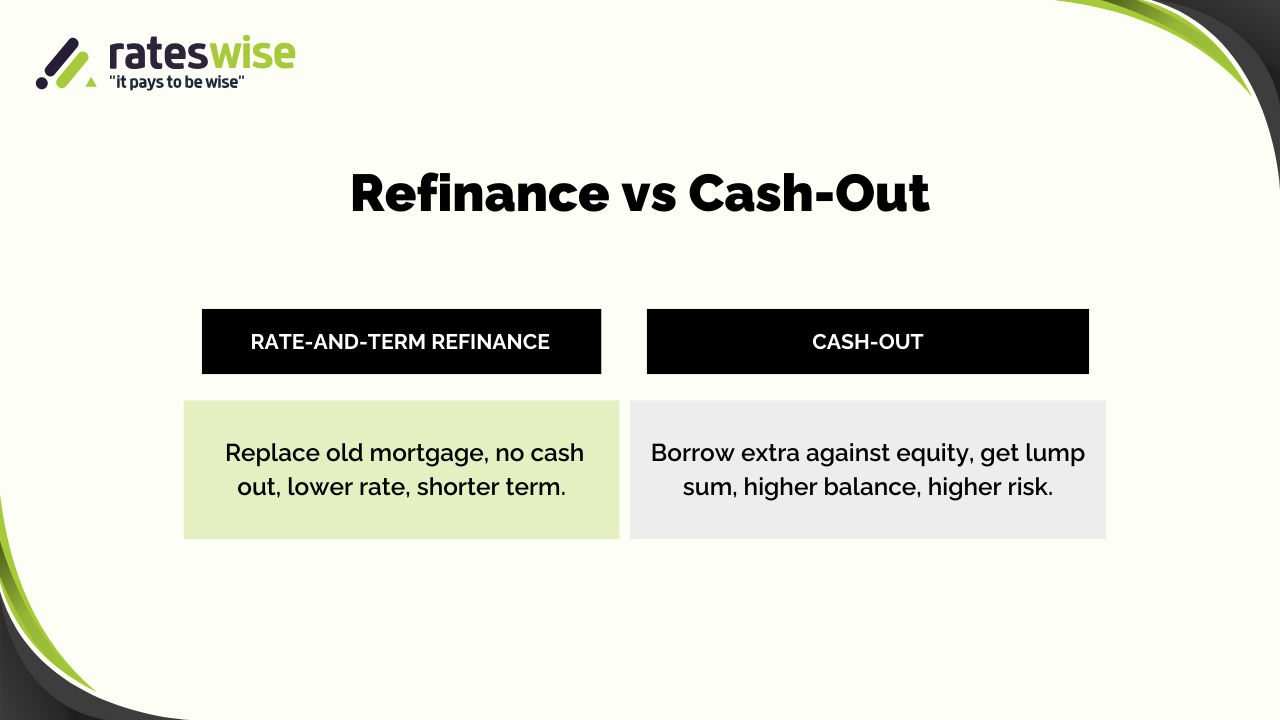

Rate-and-term vs cash-out: know the difference

- Rate-and-term: no additional funds, new mortgage replaces old. It's good to change the term or lower the rate.

- Cash-out refers to taking out a larger loan and getting the difference in cash. Excellent for large projects, but it increases the risk and balance of your mortgage.

Testimonial

I was able to compare deals with Rateswise. Each month, I saved $240. easy procedure. A Person from Ontario shared this review with us.

Alternatives to refinancing

- Renew your mortgage by staying with your lender and extending the terms when they expire.

- HELOC is an interest-only, flexible line of credit secured by equity that is accessible during the draw term.

- A second mortgage is a separate loan with different conditions that is taken out on top of your first mortgage.

- Personal loans are quicker but may have higher interest rates.

Quick checklist before you refinance

- Current mortgage term and rate

- The amount of the prepayment penalty

- Estimates of appraisal and legal fees

- Your income documents and credit score

- Examine at least three offers from lenders.

FAQs

Will my credit score suffer if I refinance?

A hard credit check could result in a slight decline. Over time, timely payments resolve it.

Can someone with poor credit refinance?

Perhaps. Rates are higher and options are more limited. Improving credit is helpful first.

In Ontario, how quickly can I refinance my mortgage?

After six to twelve months, the majority of lenders permit refinances. However, timing is crucial because if you refinance too soon, break fees may exceed savings.

Can someone with poor credit refinance?

Perhaps. Rates are higher and options are more limited. Improving credit is helpful first.

Is it possible to pay off my mortgage more quickly through refinancing?

Yes. By choosing a shorter term or a lower rate, you can allocate a larger portion of your payment to principal rather than interest.

People Also Ask

Is a rate-and-term refinance worth it?

Yes, if you intend to remain in the house for a sufficient amount of time and your new rate and term save more money than the expenses.

Does a Canadian mortgage refinance impact taxes?

It may be possible to deduct interest on a mortgage that is utilized to generate revenue, such as a rental property. Mortgage interest is typically not tax-deductible for personal expenses. Consult a tax expert.

Final note — do the math first

Rateswise team can help. Refinancing may be beneficial. Always do the math, though: savings vs fees versus penalties. It's probably worth it if the break-even point is less than the length of your stay.

Use our calculator and compare your refinance rates now!

About the Author

Written by the Rateswise Team, Canadian Mortgage Specialists

The Rateswise Team consists of seasoned mortgage professionals dedicated to helping Canadian homeowners navigate the complexities of the financial market. With years of combined experience in mortgage refinancing, home equity, and lending policies, our experts provide data-driven advice to help you secure better terms and save money. We continuously analyze Bank of Canada updates and local lender trends to ensure our guides are current, accurate, and useful for your financial journey.