Fixed vs. Variable Home Equity Loan Rates in Canada: Which Is Right for You?

June 27, 2025

As a Canadian homeowner, you can always tap into your home’s equity. Whether you’re in Ontario or elsewhere in Canada, a home equity loan can be used to pay off debt, finance educational expenses, or renovate your house.

However, it can be difficult to decide between fixed and variable home equity loan rates. Rateswise is here to make this easier, so don't worry. Thousands of Canadians have benefited from our team's assistance in locating the best mortgage options, and we're sharing our expertise to help you choose the best option for your goals and financial situation.

The equity you've accumulated over time in your house is used as collateral for home equity loans. Interest rates are lower than those of credit cards or personal loans. Many of the best home equity rates available today are less than 10% APR.

The interest rate depends on certain factors:

- Credit score

- Home Value

The total cost also depends on the interest rate you choose.

You can have a fixed or variable interest rate when you apply for a home equity loan. Variable rates change with the market, whereas fixed rates are stable. This decision affects your finances, so thoroughly weigh the advantages and disadvantages.

In this guide, we’ll explain the differences between fixed and variable rates, share a real client story, and provide you with clear steps to pick the best home equity loan in 2025.

What Is a Home Equity Loan?

You can borrow money with a home equity loan by using the equity you've accumulated in your house as security. The difference between the current value of your house and the amount you owe on your mortgage is known as equity. For example, you have $400,000 in equity if your Toronto home is worth $600,000 and you owe $200,000.

Depending on your credit score and home value, home equity loans in Canada often have interest rates lower than credit cards or personal loans; in 2025, many rates will be less than 10% APR. At Rateswise, we compare lenders for you to find you the best home equity loan rates across Canada and in Ontario.

Fixed vs. Variable Rates: What’s the Difference?

When you get a home equity loan, you’ll choose between a fixed or variable interest rate. Here’s a simple breakdown:

- Fixed Rate: Your interest rate stays the same over the entire period, and it remains the same until you pay off the debt. Your monthly payments are predictable, making budgeting easy.

- Variable Rate: Your interest rate can change based on market conditions, like the Bank of Canada’s prime rate. This means your payments may go up or down over time.

For example, Rateswise helped Sarah, a homeowner in Ottawa, choose a fixed-rate home equity loan to renovate her kitchen. “Knowing my payments wouldn’t change gave me peace of mind,” she said. “Rateswise found me a great rate, and I finished my project on budget!”

When to Choose a Fixed-Rate Home Equity Loan

A fixed-rate home equity loan is best if you want stability. Here’s when it makes sense:

- When you want to lock in a fixed rate: When you know that the cost will go up in the future. Locking in at a fixed rate helps you avoid higher costs.

- When you want to set monthly payments(budget), you need to make only fixed monthly payments over the entire period.

- When you are looking for a one-time payment, Most home equity loans come with fixed rates, and HELOCs have variable rates.

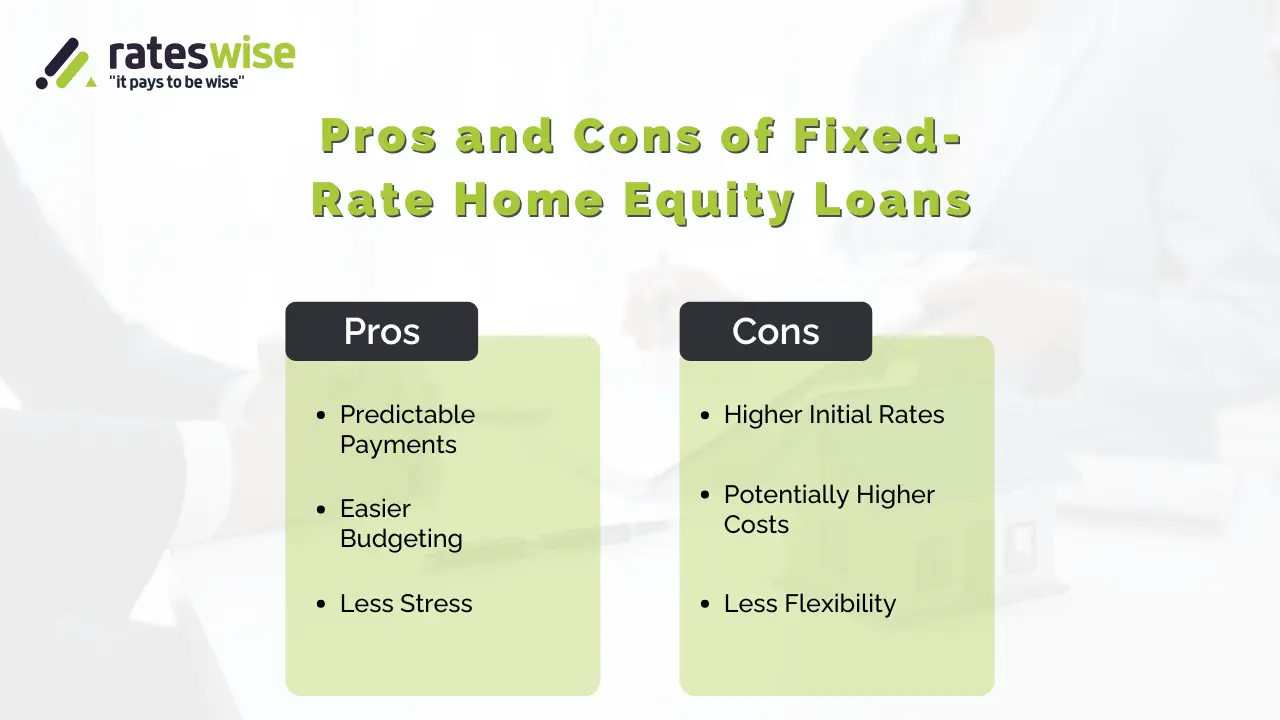

Pros:

- You know exactly how much you’ll pay every month, thanks to fixed monthly payments.

- Fixed-rate home equity loans make it simpler to plan your finances before taking out a loan.

- No surprises — your interest rate won’t change over time; it remains the same for the duration of the loan.

Cons:

- Fixed rates usually start higher, meaning you may have to pay a larger upfront amount.

- If interest rates drop in the future, you could end up paying more than someone with a HELOC or variable-rate loan.

- You won’t benefit from lower interest rates unless you choose to refinance.

RatesWise Tip: Use our free rate comparison tool to check fixed-rate options from top Canadian lenders.

When to Choose a Variable-Rate Home Equity Loan

If you can tolerate some risk, a variable-rate home equity loan, typically a Home Equity Line of Credit (HELOC) is the best option. Here’s when to consider it:

- If rates may drop: If loan rates fall, a variable rate can help you save money.

- If you're able to make adjustments to your payments, this variable rate fluctuates, so only choose this when you can handle the increase in interest rates.

- If you want a credit line: Variable-rate HELOCs allow you to borrow as much as you need and only pay interest on the amount you actually use.

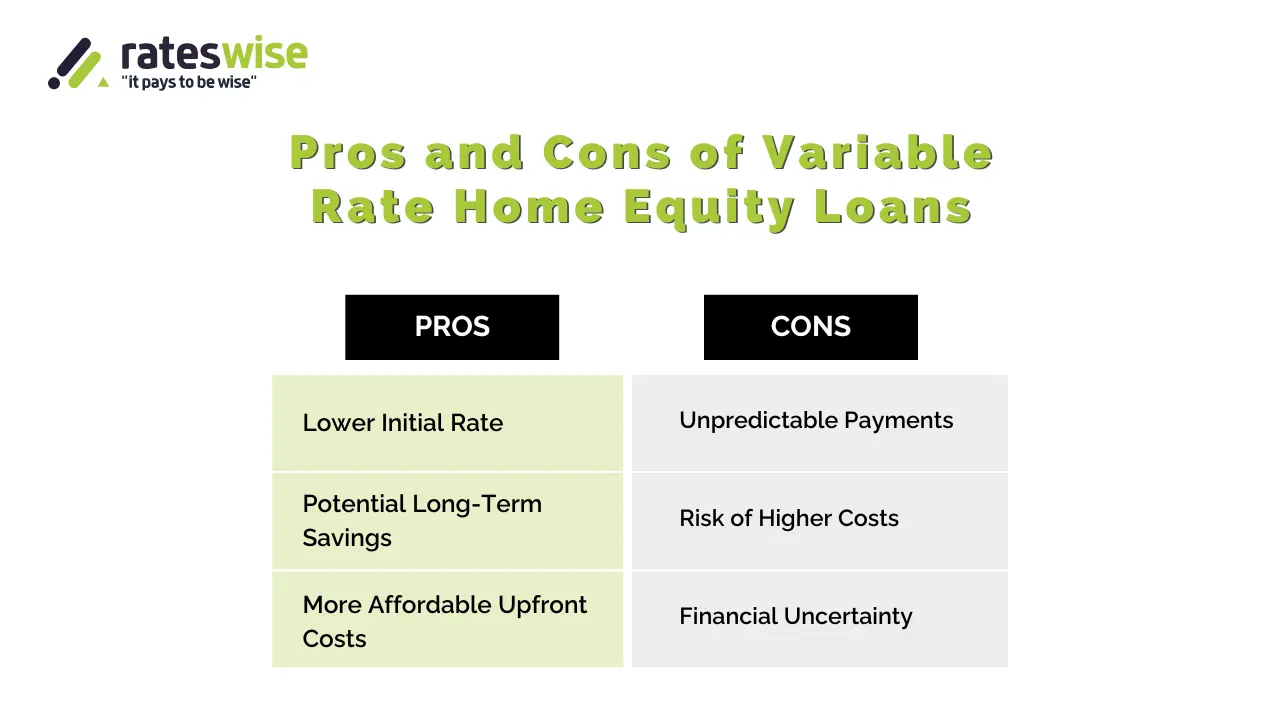

Pros:

- Typically starts at a lower rate, which can save you money early on.

- You may pay less overall if interest rates decline and stay low.

- A lower initial rate can make payments more affordable at the beginning.

Cons:

- Rates can fluctuate with the market, making it harder to budget.

- If interest rates increase, your payments could rise significantly, making it harder to pay off.

- Unexpected rate hikes can lead to unaffordable payments and negatively impact your finances.

Example: A Vancouver-based Rateswise client decided to finance his small business with a variable-rate HELOC. His payments decreased in 2024 when interest rates dropped, saving him thousands. "Rateswise found a lender that met my needs and helped me navigate the process," he said.

Which Should You Choose in 2025?

There’s no right answer to that; it depends on your financial situation and risk tolerance.

- Pick a fixed rate. If you’re looking for stable and fixed monthly payments, especially if you’re on a fixed income or budgeting for a big project in Ontario. Fixed rates are ideal for long-term loans or if you expect rates to rise.

- Pick a variable rate. If you want smaller upfront payments and are comfortable with some uncertainty, choose a variable rate. For HELOCs or shorter-term loans, it's a smart option, particularly if you can pay it off fast or anticipate a decline in interest rates.

Not sure which is best? Rateswise’s team of mortgage experts can analyze your finances and compare rates from trusted Canadian lenders.

How RatesWise Helps Canadian Homeowners

At Rateswise, we’ve helped thousands of homeowners from Toronto to Calgary to find the best home equity loan rates. With over 20 years of experience, our team of licensed mortgage brokers is here to help you at every step. We ensure you receive the best rates in 2025. We compare rates from banks, credit unions, and private lenders.

Why trust RatesWise?

- Expertise: Our brokers are experts, and they stay updated on Canada’s mortgage market, including Bank of Canada rate trends.

- Personalized Service: Whether you live in Ontario or another province, we can customise solutions to meet your needs.

- Trustworthy Advice: We prioritize transparency, without pressure and any hidden costs.

Tips to Make the Right Choice

- Check Your Credit Score: You can get lower rates if you have a higher score (e.g., 700+). Use any online tool to check your credit score.

- Compare Lenders: Rates may vary across Canadian banks and lenders. Rateswise compares lenders and simplifies everything for you.

- Consider Refinancing: You can switch to a fixed rate later if your initial variable rate declines (ask about prepayment penalties).

- Plan for 2025 Trends: Speak with a Rateswise mortgage expert to learn about market projections in light of prospective rate changes in Canada.

Conclusion

Choosing between fixed and variable home equity loan rates in Canada comes down to your budget, goals, and risk tolerance. Fixed rates offer stability for long-term planning, while variable rates can provide savings if interest rates drop. RatesWise is here to help you navigate this decision with expert advice and personalized solutions. Ready to find the best home equity loan rates in Ontario or across Canada? Get started with a free quote today!

Depending on your goals, risk tolerance, and budget, you can choose between fixed and variable home equity loan rates in Canada. Variable rates can save money when rates decline, while fixed rates provide stability for long-term planning. Rateswise offers professional guidance and personalized solutions to help you make the best decision. Are you looking for the best rates on home equity loans in Ontario or Canada? You can always reach out to us!

FAQs

What is a fixed and variable home equity loan rate?

Fixed rate: Your monthly payments are predictable because they stay the same for the duration of the loan.

Variable rate: While a variable rate depends on market conditions, like the prime rate set by the Bank of Canada, your payments could go up or down. Rateswise helps you compare the two options so you can decide which one best fits your budget.

Is a variable or fixed home equity loan better for Ontario homeowners in 2025?

It depends on your needs! If you want consistent payments, a fixed rate is best because rate hikes may occur in 2025. A variable rate, like a HELOC, is riskier, but it could save money if rates drop. Speak with Rateswise to determine which is best for you.

How can Rateswise help me find the best home equity loan rates in Canada?

Rateswise compares rates to help you find the best fixed or variable rates. Our licensed brokers, who have years of experience, walk you through the process and provide solutions to meet your financial goals, whether you're in Ontario or another province in Canada. For more information, visit rateswise.com!

Disclaimer: Lenders, credit scores, and market conditions all affect interest rates and loan terms. Always ask your lender about current details. This information is accurate as of July 2025 and is provided solely for informational purposes.

About Rateswise: Our team of licensed mortgage brokers has years of experience helping Canadians secure the best mortgage and home equity loan rates. Based in Ontario, we serve our clients nationwide and give expert advice to achieve your financial goals. Learn more at https://rateswise.com/mortgage-rates/