Understanding Home Equity Loans in Ontario, Canada: What You Should Know

September 25, 2025

Updated: September 2025

Introduction

A Canadian home equity loan can give many Ontario homeowners more financial freedom. If you need money for home improvements, to pay off high-interest debt, or to cover unexpected costs, using the equity in your home could be a good idea. But before you jump in, you need to know how home equity loans work in Canada, what lenders look for, and what the most recent changes in the market mean for 2025.

The Bank of Canada has kept its policy rate at 2.75% since July, which means that borrowing costs have stayed pretty stable compared to the highs of 2024–2025. This has made home equity loans in Ontario more appealing again, especially for families with high credit card balances (which are usually between 19% and 29%).

We'll go over how to get a home equity loan, the pros and cons, and how Rateswise helps Ontario homeowners find the best home equity loans that Ontario lenders can offer.

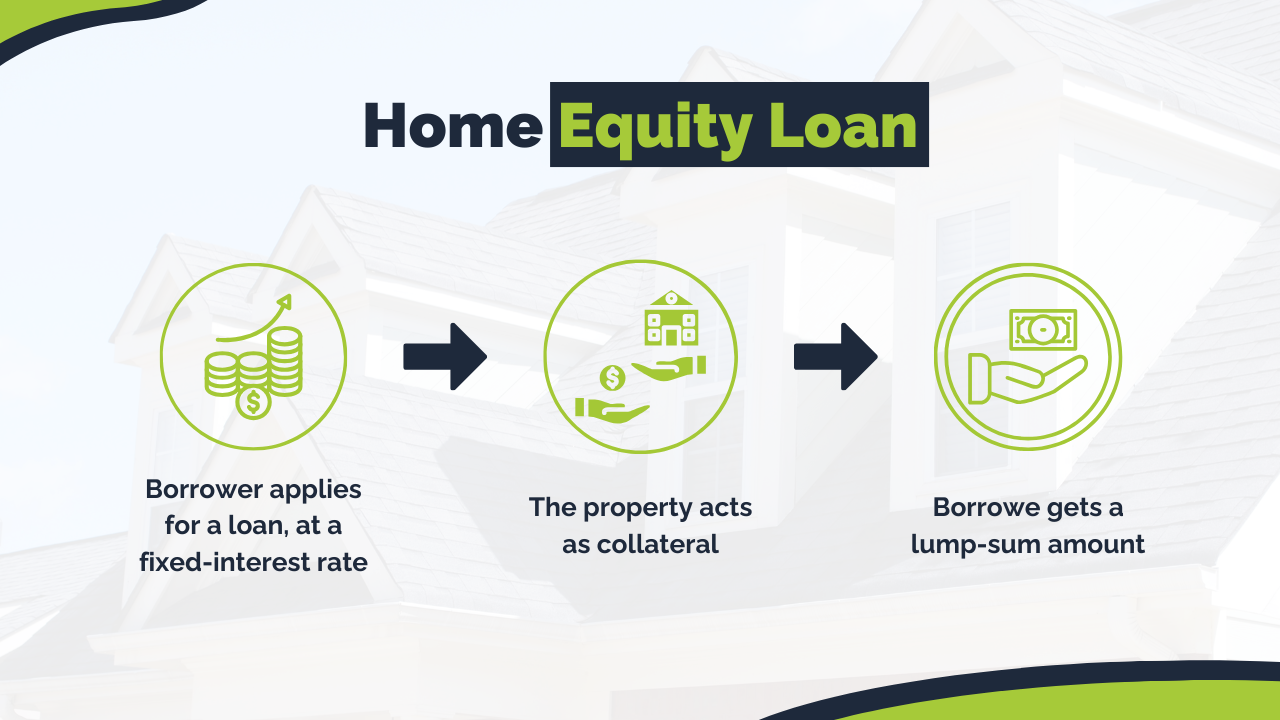

What Is a Home Equity Loan in Canada?

Taking out a loan against the value of your house is known as a home equity loan. The majority of lenders in Canada will let you borrow up to 80% of the assessed value of your house, less the remaining mortgage balance.

Example:

- Value of home: $800,000.

- $400,000 is the mortgage balance.

- $640,000 is the value at 80%.

- $240,000 is the amount of available equity.

With about $240,000 in equity, you might be eligible for a loan.

Why Ontario Homeowners Use Home Equity Loans

In Ontario, home equity loans are commonly used by homeowners for

- Debt consolidation: repaying personal loans or credit cards with high interest rates.

- Home renovations: to upgrade the kitchen, basement, or energy upgrades.

- Education: Covering tuition costs for children or yourself.

- Investments: Funding a business or investment opportunity.

Many homeowners in Ontario have a substantial amount of equity available because the average home price in 2025 is still close to $850,000 (CREA, August 2025).

How to Apply for a Home Equity Loan in Ontario

Qualifying for a first mortgage is more complicated than getting approved for a home equity loan. Lenders will look at:

- Available home equity (up to 80%)

- Credit score (often 650 or above)

- Income stability (reliable employment or business)

- Ratio of debt to income

How to Apply:

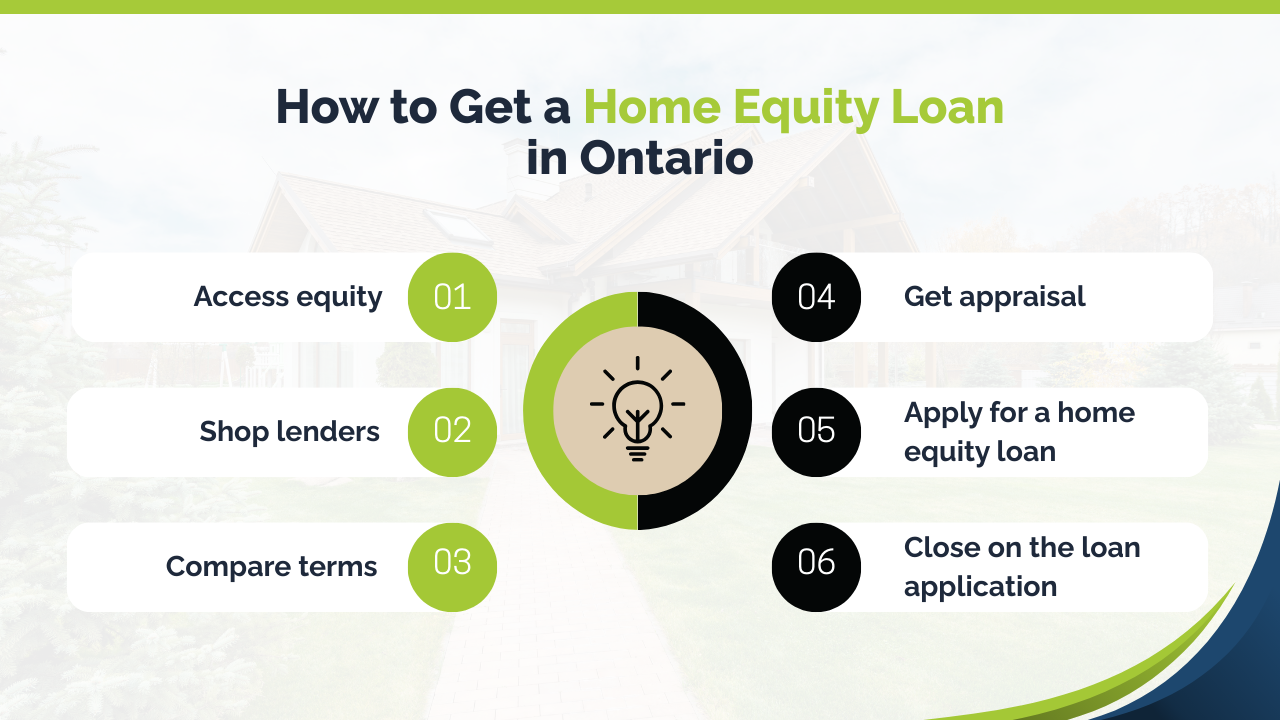

- Assess your equity: Calculate using the home's value and the mortgage balance.

- Shop lenders: Banks, credit unions, and mortgage brokers in Ontario.

- Compare rates: Look at fixed and variable rates.

- Get an appraisal: Lenders require a current home appraisal.

- Provide documentation of your income, debts, and mortgage information when you apply.

Best Home Equity Loans Ontario: What to Look For

Loans are not all made equal. Homeowners in Ontario should compare:

- Interest rates: Fixed rates provide stability, while variable rates may be lower.

- Fees: Set-up, legal, and appraisal costs can mount up.

- Terms of prepayment: Verify penalties for early repayment.

- Flexibility: Rather than offering lump sum payments, some lenders provide credit lines.

Rateswise matches you with the finest home equity loan that Ontario homeowners are eligible for based on your financial circumstances by collaborating with lenders.

Pros and Cons of Home Equity Loans

Pros

- Usually have lower interest rates compared to personal loans and credit cards

- Large loan sums are accessible.

- Fixed (predictable) payments

- Money can be utilized for anything.

Cons

- Your house serves as collateral (foreclosure risk).

- Fees and closing expenses

- Variable loans may see an increase in interest rates.

- More interest is charged over longer repayment durations.

Is Now a Good Time in Ontario?

Yes, however, it will depend on what you're looking for. Borrowing costs are low in comparison to previous years since the Bank of Canada has maintained its policy rate at 2.75%. A home equity loan at 4.5% to 6% could save you thousands of dollars a year if you're consolidating debt with interest rates of 20% or higher.

Homeowners should consider the risks involved, though, as they may lose their equity or even their house if housing values decline or they default.

Testimonials

“I had no idea I could qualify, but the team walked me through everything. Now I’ve got funds to renovate my basement.”

FAQs

In Canada, what is a home equity loan?

This kind of loan allows you to borrow against your home's equity, typically up to 80% of its assessed value.

In Ontario, how can I be eligible for a home equity loan?

You must have sufficient equity in your home, a reliable source of income, and decent credit.

Are HELOCs inferior to home equity loans?

HELOCs are variable lines of credit, whereas loans provide you with a single sum with fixed payments.

Can I use a home equity loan to buy another property?

Yes, many investors in Ontario utilize them for rental properties or second homes.

Are you looking for the best home equity loans in Ontario? Use the Rateswise calculator and check your eligibility now.

Disclaimer

Lenders have different requirements for mortgages and loans, and interest rates might fluctuate. Before making any financial decisions, always get advice from a qualified mortgage advisor.

About the Author

Written by the Rateswise Team

At Rateswise, we have assisted hundreds of families in Canada in using their home equity for future investments, renovations, or debt repayment.