5 key factors that determine your home equity loan rate

May 13, 2025

Updated July 2025

What are home equity loans?

When you take a home equity loan, you can access equity. The amount you borrow is determined by your income and credit score. It is limited to 80% of your equity. You get the one-time lump sum money, and you have to pay it back with regular monthly installments over time. Your home acts as collateral when you default on the loan. Home equity loans have fixed interest rates.

There are 2 conditions:

A home equity loan with fixed rates has the same interest rate over the entire period.

Fixed-rate home equity loans are better for borrowers who value consistency. Home equity loans with variable rates may increase or decrease with time. Variable-rate loans could be a better option for short-term borrowing due to their lower initial interest rates.

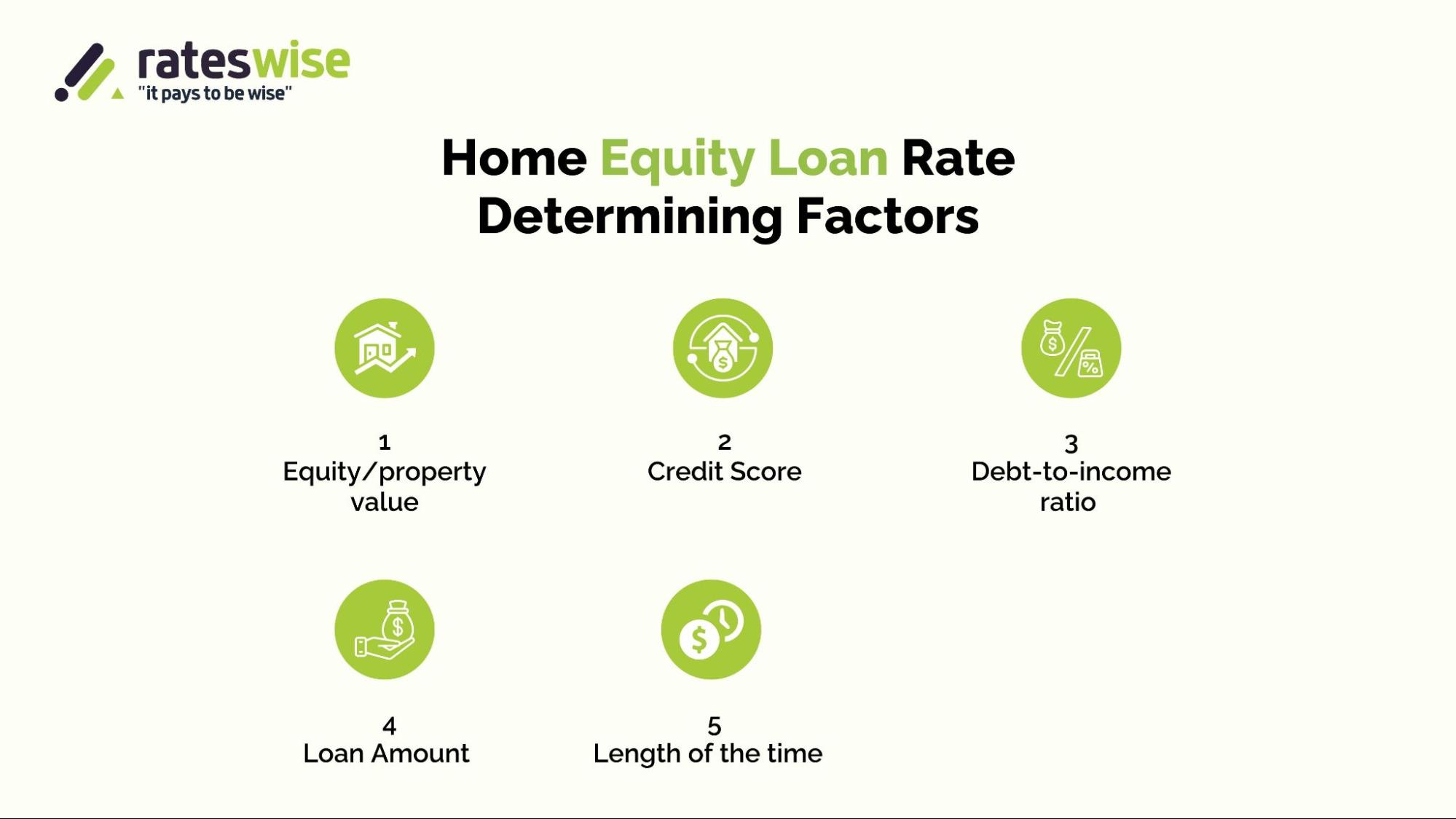

Home equity loan rate determining factors

You must learn about how much you need to borrow and how to do it if you intend to use a home equity loan for these reasons: home improvements or debt repayment. You can apply for a home equity loan by using your home equity.

Understanding these things helps you get the best rate. Here are the five main key factors:

1- Equity/property value

2- Credit Score

4- Loan Amount

5- Duration of the period

1- Equity or Property Value

The major factor in applying for a mortgage is your property value. Ask an expert home appraiser to verify your home’s value.

You need to be aware of your home's equity in order to lend and borrow money. In essence, equity is the difference between the value of your home and the mortgage balance. When you have more equity in your home, the less expensive it will be for you to borrow money, because the lenders will feel more secure.

2- Credit Score

Lenders look at your credit score to check how accountable you are with debt. It is an important factor to see whether you get approved or denied to take out a loan.

A higher credit score of 700+ may get you a lower interest rate, similarly with a lower credit score could result in higher rates.

It could be a smart choice to get a short-term loan to raise your credit score, particularly if it enables you to receive a better interest rate on a longer-term loan after your credit has been restored.

A quick update:

In June 2025, the Bank of Canada kept its policy rate at 4.25%. Lenders are giving credit scores and loan-to-value ratios greater weight, and home equity loan rates are still higher than they were before 2023. For competitive rates, it is still best to maintain a 700+ score and stay below 80% LTV.

3- Debt-to-income ratio

Lenders look at your income and overall debt to ensure you can repay the loan. You have a better chance of getting a low interest rate if you have a stable income and a low debt-to-income ratio.

No matter how much equity you have in your home, interest rates will be higher than you anticipated if you apply for a mortgage without a job.

Like credit loans, it could make sense to take out a small home equity loan while you're looking for work or launching a small business.

Lenders are more willing to provide you with the preferred rates for low-risk borrowers when you meet the income requirements.

4- Loan Amount

Think about taking out a loan in a few steps. Rebuilding your income and credit will allow you to borrow money at lower rates later on. If you currently have a weak credit application or credit score, you should only take out loans for immediate expenses.

5- Duration of the period:

The length of time you need to borrow the money matters. Short-term loans with higher rates and lower fees might be sensible for someone who just needs the money for a short period of time.

However, a borrower looking for a longer-term solution would consider paying a break penalty or a charge to get a lower interest rate for a longer period of time, which would ultimately save tens of thousands of dollars in insurance costs.

Final Thoughts

Your credit score, loan amount, financial status, length of time, debt-to-income ratio, and lender all affect your home equity loan rate. Reduce your debt, raise your credit score, and research offers to get the best deal in Canada.

FAQs

In Canada, what would be a reasonable home equity loan interest rate in 2025?

Competitive rates as of July 2025 range from 6.5% to 8.25%, based on equity and credit score.

Can someone in Canada with poor credit get a home equity loan?

Yes, but the terms would be difficult to manage, and you’ll pay a higher rate. Think about getting a co-signer or enhancing your credit.

How much equity do I need to get a loan in Ontario?

Mostly lenders required that you have at least 20% equity left in your house after the loan (an LTV of 80% or less).

Is a HELOC better than a home equity loan in 2025?

Home equity loans have set payments, while a HELOC offers flexibility with variable rates. Your needs will determine this.

Does inflation impact home equity loan rates?

Yes. Interest rates are affected by the Bank of Canada's policy decisions, which are influenced by inflation.

Are you ready to explore your options? Compare home equity loan rates based on your credit profile and get matched with top lenders. Learn more about home equity loan rates.

Disclaimer: This content is based on current facts and intended purely for informational purposes. Always ask your lender about current details.

About the Author

Written by the Rateswise Team

The Rateswise Team consists of financial analysts and mortgage experts who specialize in the Canadian home equity market. We are dedicated to demystifying the lending process by breaking down the key factors that determine your interest rate. This guide reflects our deep understanding of how lenders assess risk—from credit scores to debt-to-income ratios—and our commitment to empowering you with the knowledge needed to secure the most favorable loan terms possible.