HELOC vs Home Equity Loan: What’s the Best Option for You in 2025?

June 24, 2025

As a homeowner, if you’re looking to borrow some funds, you might wonder which loan is good for you. What is the difference between a home equity line of credit and a home equity loan?

Homeowners can use the equity in their houses to get additional funds at low interest rates through both home equity loans and HELOCs. Make sure you choose the loan that meets your needs and lifestyle.

Let’s see how these two differ.

What is a Home equity loan and HELOC?

Requirements Vary for Both

For a Home Equity Loan

A home equity loan process can take a long time, and approval is not always guaranteed. Lenders will review your financial situation to evaluate whether you are qualified for this. They will look into your credit history, credit reports, borrowing history, and your home appraisal. They will also assess your ability to repay the loan, just like they would with any other loan. Lenders will also consider the following factors while assessing your application:

Home equity: At least 15–25% of the value of your house must be yours. Your home will be appraised by a lender, usually at your expense.

Debt-to-income ratio: This calculates how much income is spent on debt. Lenders prefer a DTI under 43%, it doesn’t exceed a certain amount. They can also ask to provide pay stubs, W-2s, and tax documents.

Credit Score: You have a better probability of getting approved if your credit score is high. Most lenders ask for 650+ or 700+, maybe. This can also help you get better interest rates.

For Home Equity Line of Credit (HELOC)

The application is similar to the home equity loan. Lenders will evaluate your financial history and home appraisal to see if you qualify for this loan.

They will also consider the following elements:

Home Equity: You must have accumulated equity in your residence. How much you can borrow against your equity and how much you have accumulated will determine this.

Debt-to-Income Ratio: For HELOC, most lenders review your existing debt and income. You may be required to provide evidence of your employment or income.

Credit History: A high credit score increases your chances of being approved, just like it does for a home equity loan. Lenders might review your credit reports and borrowing history. If you get approved, you may get a credit card for a HELOC. Always remember to review the terms, as repayment rules may vary.

Which one is better for you?

Now that you know these options differ, you can decide which loan works best for you that meet your needs.

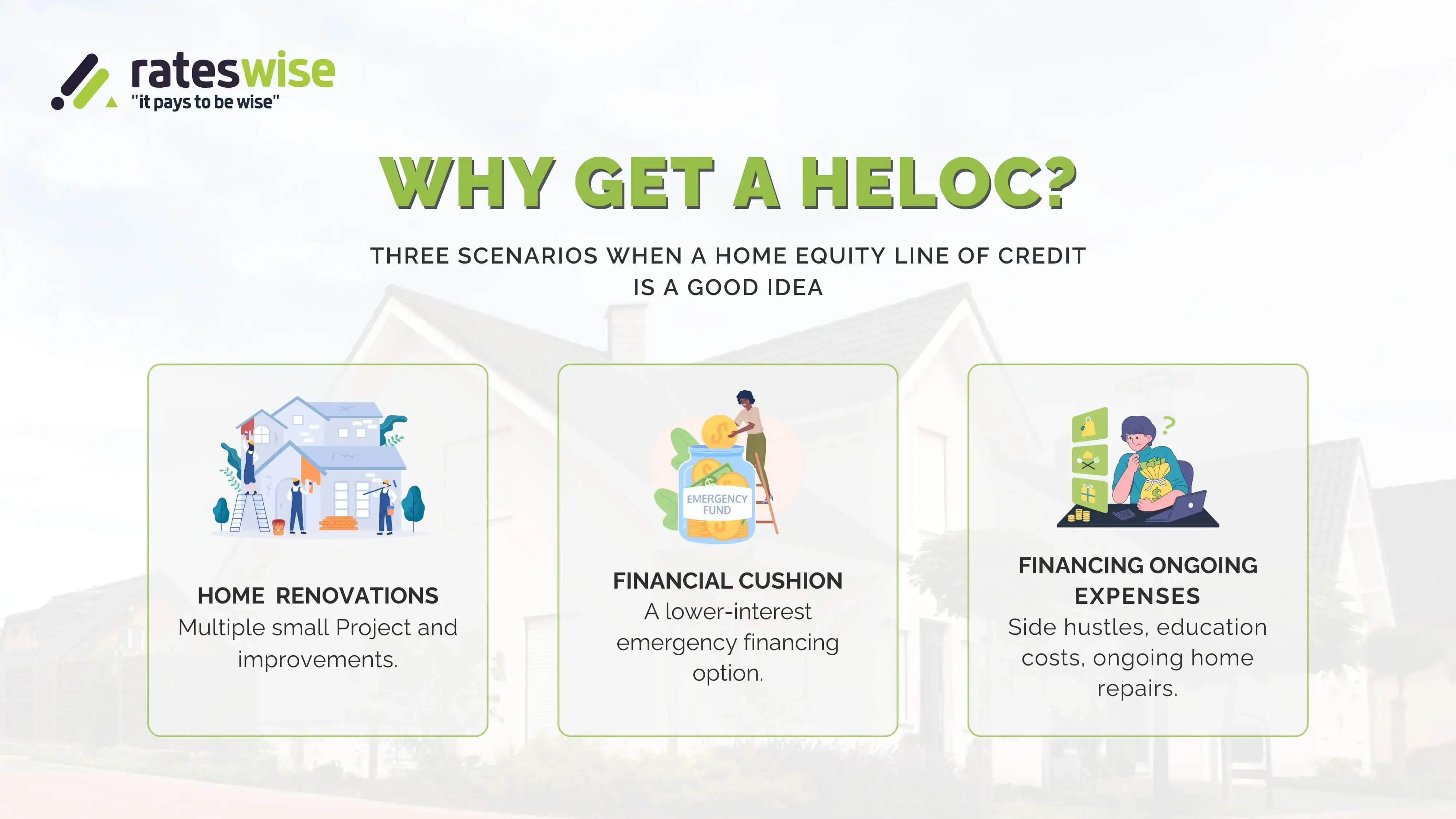

HELOC might be good for you if:

- If you’re planning to start an ongoing project that will take time, HELOC is an excellent option. You only pay interest on the amount you use. For example, if you’re planning to renovate the kitchen and bathroom in the future, a revolving line of credit (HELOC) could be a perfect fit.

- You can consolidate your debt, a higher-interest credit card, or loan payments into a single monthly payment.

- You can borrow as much or as little as you need, according to your credit limit. As it offers this much flexibility, it is an excellent choice for a rainy-day fund.

A Home Equity Loan might be good for you if:

This is a good option for larger or one-time expenses. For example, home renovation.

You have fixed monthly payments over the term. The terms of home equity loans range from five to twenty years, and their interest rates are usually fixed. You’ll feel secure because you know that your monthly payments stay the same.

Like a HELOC you want to consolidate your loan. A home equity loan is a viable option to balance transfers and high-interest loans.

HELOC Vs Home Equity Loan

Vs Home Equity Loan.webp)

Both have some similarities as well like they both need the equity you’ve built in your property. There are also key differences involved; let’s discuss that in detail:

How it works?

HELOC

You can Borrow funds as much as you need up to the credit limit

- Credit limit(for 10 years) is also known as the draw period. Pay interest on only what you use. Repay the used balance. After that, the repayment period starts in which you’ll repay your outstanding balance over the next 20 years.

Home Equity Loan

You can borrow a one-time lump sum amount/fund

- Repay it according to a fixed term at a fixed rate. You can estimate the fixed monthly payments.

Features of using home equity for

HELOC

- Low, variable rate

- Option to lock your interest rate

- Most of the time, there are no closing expenses

Home Equity Loan

- A low and fixed rate

- Choose a plan that fits your budget with terms from 5 to 30 years

- Most of the time, there are no closing expenses

Interest Rates

HELOC

Variable interest rate

- APR is a variable interest rate that is linked to the prime rate, plus an extra percentage on the location and condition of your home, the loan amount, and your credit history. Some lenders offer you to lock in at a fixed rate, because interest may vary during the draw period.

Home Equity Loan

Fixed interest rate

- Your monthly payments and interest rate remain fixed during the entire loan term. It depends on certain things: the condition and location of your home, your credit history, and the loan amount.

Term

For HELOC:

- It will be divided into draw and repayment periods.

- 30-year HELOC term: 10-year interest-only draw period + 20-year repayment period.

For Home Equity Loan:

- Pick your loan term (typically anywhere from five to 20 years).

- Options with terms of 5, 10, 15, 20, and 30 years

- You'll make principal and interest payments.

Repayment

HELOC: You need to pay interest during the draw period only. Also, during the repayment period, you’ll make monthly payments (principal + interest)

Home Equity Loan: You need to make payments, principal and interest throughout your term.

Maximum combined loan-to-value % (CLTV):

For HELOC and Home equity loan: Up to 89.99% of the home's value

Pros and Cons Of HELOC and Home Equity Loan

HELOC

There are various pros and Cons for HELOC; you need to consider these things before you make any decision.

Pros of HELOC (Home Equity Line of Credit)

- It’s easy to access funds when needed, up to the credit limit.

- Because HELOCs are variable, you can adjust them to suit your borrowing needs.

- Interest rates are usually lower than unsecured loans or credit lines.

- You pay interest only on the amount you actually use.

- You can repay at any time during your loan term without any penalt

- It can be useful to consolidate debt.

Cons of HELOC

- Because of variable rates, your payments could rise anytime.

- You need to be financially stable to manage the loan. In some cases, you make interest-only payments in the beginning.

- You must avoid using a HELOC for everyday or unnecessary spending to avoid long-term debt.

- It is difficult to switch lenders, as not all lenders offer HELOCs—this can result in higher mortgage rates.

- Failure to make payments on time may lead to the power of sale or foreclosure.

- Your lender has the right to recall the HELOC and demand full repayment at any time.

- If you fail to make minimum payments, it can negatively affect your credit score.

Home Equity Loan:

Let’s see what pros are for a Home equity loan; they have some Cons as well, have a look:

Pros of Home Equity Loan

- Since the payments are amortized, that helps you pay off your debt on time.

- You can use the money for any purpose, such as home renovations, education, or a down payment for your child’s first home.

- Home equity loans typically have lower interest rates than personal loans or credit cards.

- Lender approval is based more on your home’s equity than your credit score—if you have good equity, you may qualify for more.

- There are no penalties if you get the loan from your current lender.

- Fixed interest rates make repayments predictable and easier to manage.

Cons of Home Equity Loan

- Home equity loans usually have higher upfront costs than personal loans.

- Late payments can result in foreclosure, as your home is used as collateral.

- Less flexibility—you can’t withdraw smaller amounts as needed, like with a HELOC.

Frequently Asked Questions

Q. What is the difference between a HELOC and a Home Equity Loan?

A HELOC is a revolving line of credit with variable interest rates, while a Home Equity Loan is a one-time lump sum with fixed payments and a fixed interest rate.

Q. Which one is cheaper right now?

At the moment, both are nearly the same, around 8.26–8.27% average interest rate. If rates drop, the HELOC could save you money, but it could also go up.

Q. How much equity do I need to qualify for a HELOC or Home Equity Loan?

Most lenders require you to have at least 15–20% equity in your home to qualify, though some may accept slightly less depending on credit and income.

Q. Will a HELOC or Home Equity Loan affect my credit score?

Yes. Both loans are reported to credit bureaus. On-time payments can help your score, while missed payments can hurt it. A HELOC may also affect your credit utilization ratio.

Q. Can I use these loans to pay credit-card debt?

Yes. Many homeowners use HELOCs to pay off high-interest cards; the average credit card interest is over 20%, while HELOCs are about 8.27%. Just keep in mind you’re using your home as collateral.

Q. Are HELOC interest payments tax-deductible?

Only if you use the money to improve your home, and only up to certain limits.

People Also Ask

How much can I borrow with a HELOC or home equity loan?

Lenders usually allow you to borrow up to 80–85% of your home’s value (after subtracting your current mortgage).

How much would a $100,000 HELOC cost per month?

At today’s rates (8.26%), you’d pay roughly $1,227 over 10 years or about $971 over 15 years.

About the Author

Written by the Rateswise Team

We’re a group of mortgage experts and writers who simplify difficult subjects into simple terms. We're here to help you understand your options, compare rates, and make a smart choice.

Disclaimer: This content is based on current facts and intended purely for informational purposes. Always ask your lender about current details.