Reverse Mortgages in Canada: What You Need to Know

November 21, 2025

Updated: November 2025

Introduction

With a reverse mortgage, Canadian homeowners (often those over 55) can access cash by using their home equity without having to make monthly payments. This option is becoming more and more popular, particularly among seniors who want to increase their income while remaining in their homes. It's not for everyone, though. We go over how reverse mortgages operate in Canada, how rates are calculated, and the risks involved in this guide.

How a Reverse Mortgage Works in Canada

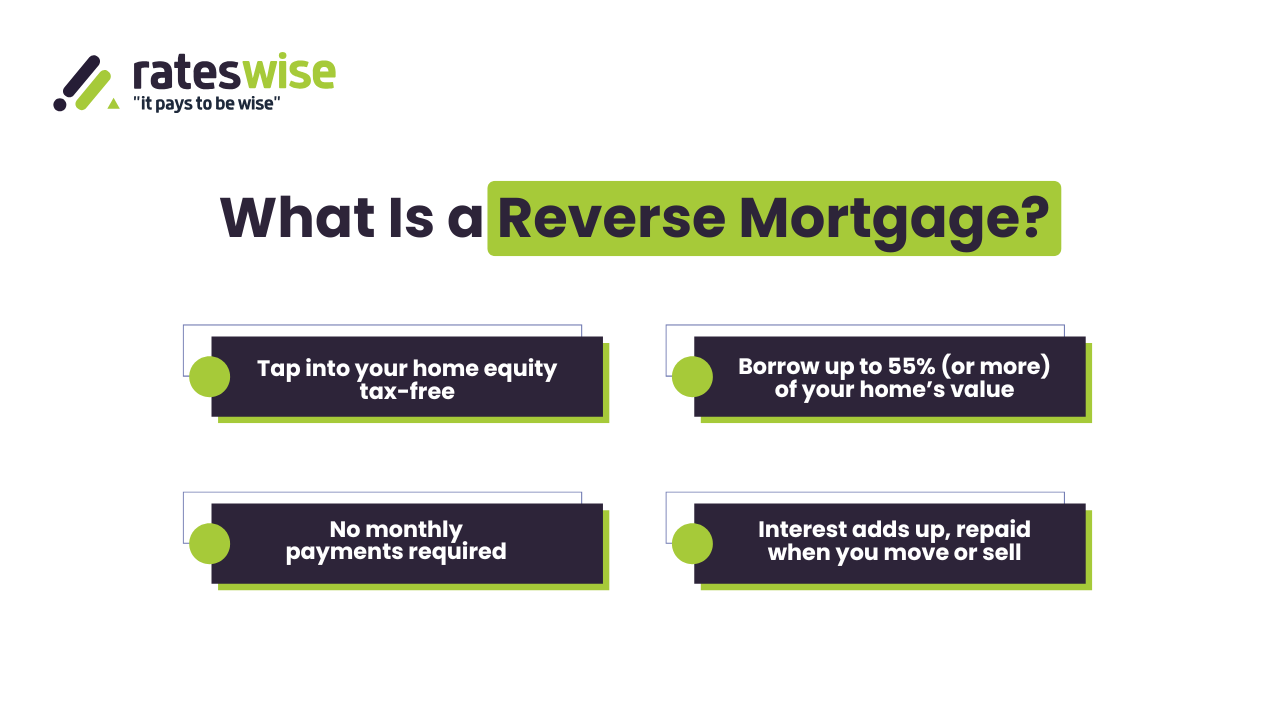

- You take out a loan against the value of your house when you have a reverse mortgage. We refer to it as "equity release."

- The interest you owe is gradually added to the loan total; you do not make monthly mortgage payments.

The money can be given to you as:

A one-time payment,

monthly or quarterly payments on a regular basis, or

Both of them combined.

- Usually, you have to pay back the loan when you sell the house, move out permanently, or die.

Canadian Policy & Eligibility (2025)

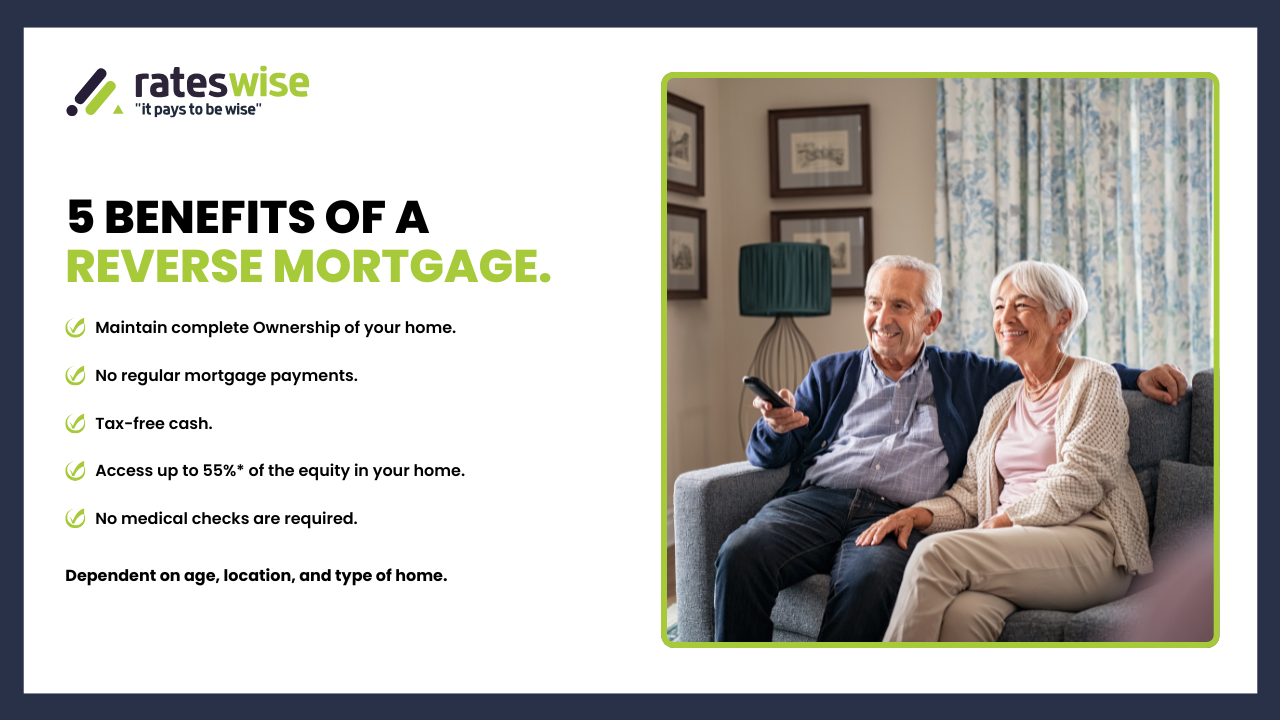

- Typically, you need to be at least 55 to be eligible.

- You must live in the property for at least six months out of the year, making it your primary residence.

- Depending on the lender, you might be able to borrow up to 55% (or even 59%), of the value of your house.

- Age, home worth, and condition all affect the precise amount.

- Important: Generally, you have to pay off any outstanding mortgages or HELOCs first.

How do prices and rates work?

Interest rates on reverse mortgages are typically higher than those on HELOCs or regular mortgages.

Here are some examples:

- The 5-year fixed rates for HomeEquity Bank's CHIP reverse mortgage range from roughly 6 to 7%, depending on the type.

- With Equitable Bank's reverse mortgage program, borrowers can get up to 59% of the value of their home and are guaranteed "no negative equity."

- Watch out for these fees: closing, legal, setup, and appraisal costs may be added to the loan and grow over time.

Pros & Risks of Reverse Mortgage

Pros:

- You can get money without selling your house.

- You can choose whether or not to make a payment each month.

- Helps pay off debt, fix up the house, or save for retirement.

Risks:

- Your debt grows over time because of compound interest.

- Your home's equity could go down, which would leave you with fewer assets to leave behind.

- When you or your estate pays it back, the remaining amount could be large.

- Not all homes are eligible for loans, so your home needs to meet the requirements.

Reverse Mortgage vs HELOC / Second Mortgage

- Although you have flexibility with a home equity line of credit (HELOC) and only pay when you borrow, you still have to make regular payments.

- With a reverse mortgage, you receive cash up front, but you pay off the remainder over time.

- Reverse mortgages don't need monthly payments like second mortgages do, but the total amount owed might still add up.

Example

There is a homeowner who shared his story that his house in Ontario is worth $400,000.

He is eligible to borrow up to 55% of the value (around $220,000) through a reverse mortgage. In order to pay off his HELOC and pay for medical expenses, he takes out a $100,000 lump sum.

He doesn't have any monthly payments due. Interest accrues during a ten-year period, yet he remains in the house. The loan is paid back from the sale when he moves or sells.

know the

FAQs

How can I figure out how much equity a reverse mortgage will allow me to access?

A reverse mortgage calculator is provided by many reverse mortgage lenders. To determine how much you can borrow, just enter your age, projected rate, and house value.

Will my credit score be impacted by a reverse mortgage?

Regular credit reporting is usually absent when there are no monthly payments. On the title, nevertheless, the reverse mortgage is visible.

Is it possible to replace or refinance a reverse mortgage?

Theoretically, yes, but because the debt has increased and the equity may be reduced, it is challenging to convert it into a conventional mortgage or HELOC.

Disclaimer

This blog is intended only for educational purposes. Due to the complexity of reverse mortgages, you should always get legal and mortgage professional advice before making any decisions.

About the Author

Written by the Rateswise Team

Experienced Canadian mortgage experts who help homeowners make informed decisions about home equity, retirement planning, and reverse mortgage options across Canada.