Refinance or Not? How a Mortgage Calculator Reveals What’s Right for You in 2025

October 27, 2025

Updated: September 2025

Introduction

Are you considering a mortgage refinance in Ontario or elsewhere in Canada? You can use a refinance home mortgage calculator to prevent you from being caught off guard; it assists you in estimating how your payments would appear under various interest rates and terms. Many lenders are reducing their variable and fixed refinance offers in 2025 after the Bank of Canada lowered its policy rate to 2.50% on September 17. Before you make decisions, let's examine how this calculator functions, what it displays, and how to use it with confidence.

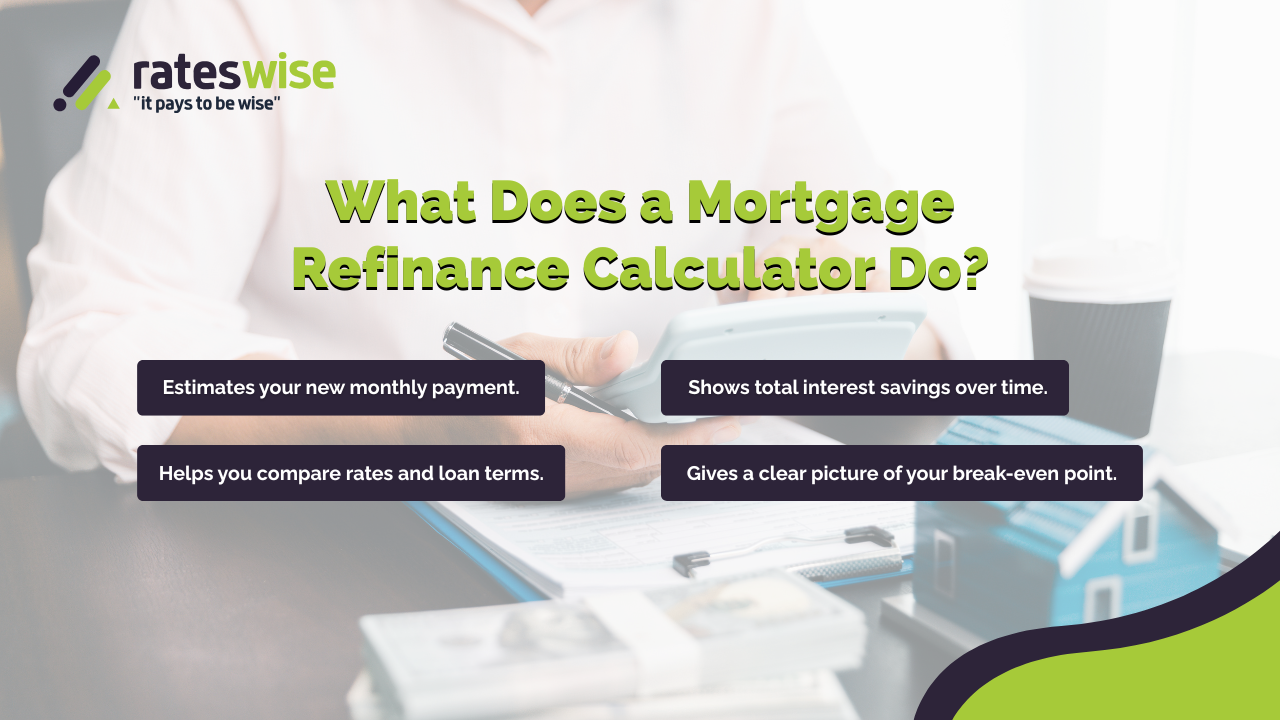

What Does a Mortgage Refinance Calculator Do?

A refinance calculator displays the following after receiving your existing mortgage balance, interest rate, remaining term, and the new proposed rate/term:

- Your updated monthly installment

- The amount of interest you will pay more or save

- The break-even point (the number of months it will take to recover the cost)

- Total expense for the duration of the loan

You can test scenarios by using terms such as mortgage rate for refinance or rates for refinance. For example, "What if I drop the rate by 0.5%?" or "What if I shorten the term?”

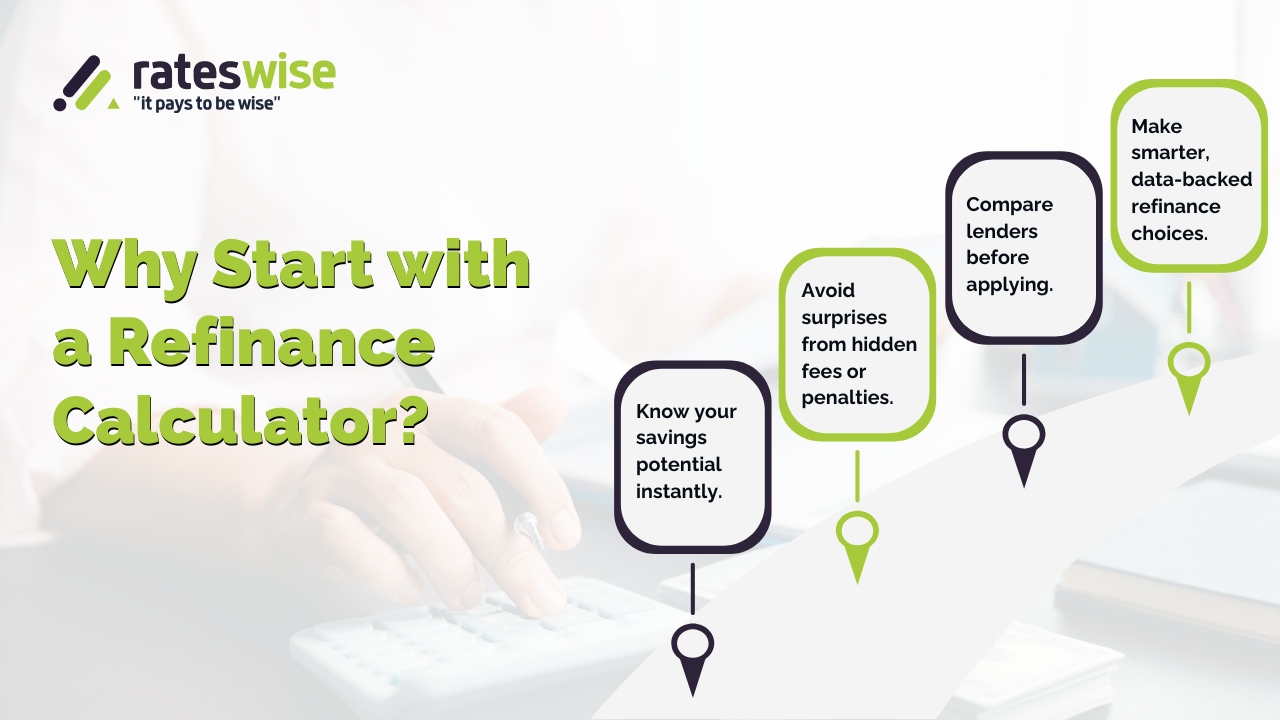

Why start with a Refinance Calculator?

- To avoid surprises —Know your new payment before applying

- Compare offers — See the prices of two distinct lender proposals side by side

- Determine if it’s worth it - examine whether fees and penalties will eliminate your savings.

- Plan your timing — Use a calculator to simulate waiting vs acting right away, if the rates are declining.

Example:

Following the BoC cut, some brokerages offered fixed refinance rates of about 4.15% in the summer of 2025. Rateswise Refinance Calculator may indicate that you save $200 per month if your current mortgage rate is 5.0%, but if your penalty is $3,000, it might be better to wait.

Canada Refi Findings (2025 Latest Updates)

- The Bank of Canada reduced its policy rate from 2.75% to 2.50% on September 17, 2025.

- Prior to that, it had made several announcements to keep the rate at 2.75%.

- Many lenders started reducing variable refinance mortgage rates after that cut. A few fixed refinance offers that were posted fell to 3.9% or more.

- A BoC staff note states that payment increases are anticipated for roughly 60% of mortgage holders renewing in 2025–2026 (particularly those in 5-year fixed deals).

Because of these changes, it's even more crucial to use a refinance calculator to see if your anticipated savings will hold up against rate adjustments and penalties.

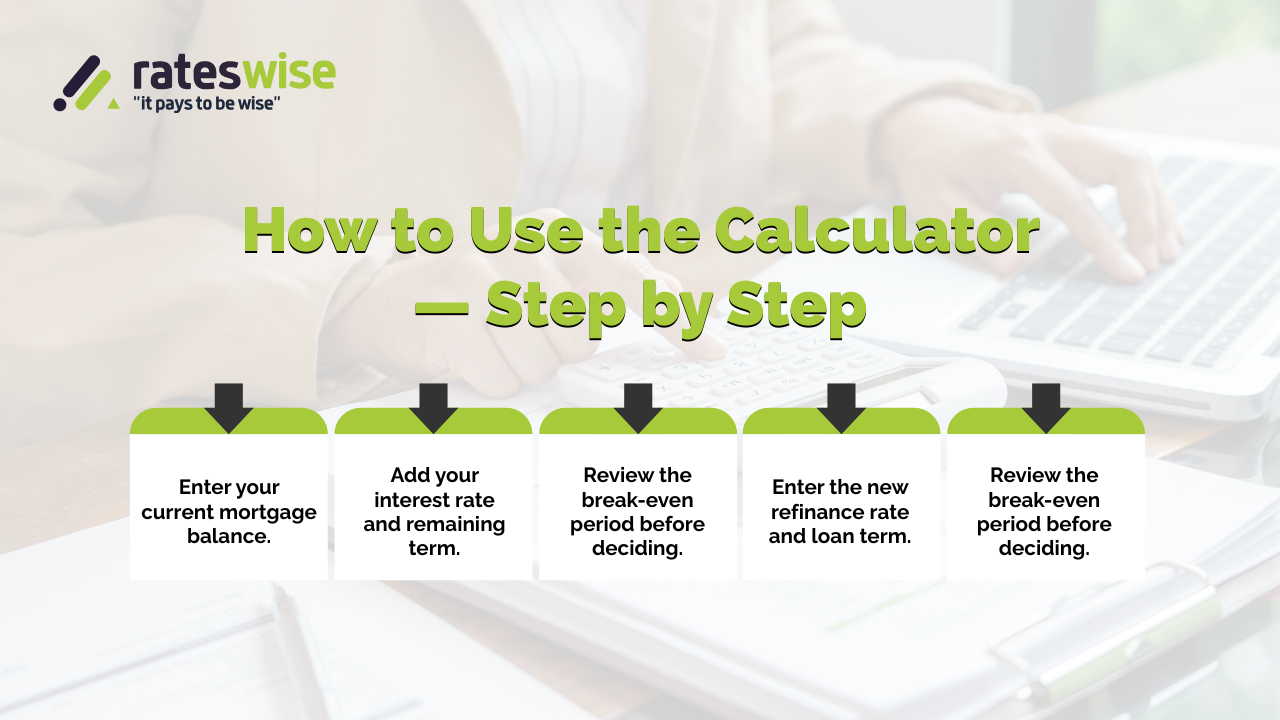

How to Use the Calculator — Step by Step

Here are some steps that one should take and why they matter:

step 1

Current mortgage balance - It matters because of the baseline for comparison

step 2

Current rate & remaining term- For accurate projection

step 3

Proposed new rate & term options- To test scenarios

step 4

Penalty, closing costs, fees- To factor in hidden costs

step 5

Run simulation- Compare payments, interest, and break-even

You can run these scenarios manually to verify what lenders display, or you can use the Rateswise refinance calculator to do it quickly.

Case Study of an Ontario Homeowner

A homeowner in Mississauga, Ontario, had a $350,000 mortgage balance with ten years remaining at a 4.8% interest rate. She entered the following refinance rate: 4.0% over 7 years.

- $1,900 is the new monthly payment

- Former payment: about $2,150

- Savings per month: about $250

- Fees plus penalty: $4,000.

- Breakeven point: about 16 months

Refinancing made sense because she intended to stay for 3+ years. Before speaking with lenders, Lina felt more confident thanks to the calculator.

FAQs

1. What is a mortgage refinance calculator, and how does it work?

Before refinancing, you can estimate your new payments, interest savings, and break-even point with the help of a mortgage refinance calculator. This shows you how much you could save over time if you just enter your loan balance, current rate, and new offer. Comparing lenders before applying is made simpler as a result.

2. Why should I use a refinance calculator before applying?

Because it helps you to see things clearly. It indicates if, after deducting closing costs, penalties, or fees, refinancing will truly result in cost savings. After the BoC's rate changes in 2025, many homeowners in Ontario use it to determine whether it makes sense to move from a 5.5% to a 4.8% rate.

3. Are refinance calculators accurate?

They're not a final quote, but they're a great place to start. While actual offers are determined by your income, credit score, and lender risk assessments, calculators only provide estimates based on your values. For accurate numbers, always confirm results with a mortgage expert.

The quality of your input determines how close they are. Always double-check with your lender to confirm.

4. How can I use a calculator to find the best refinance rates?

Do several comparisons. Enter various loan durations (such as three or five years) and compare fixed and variable rates. Test "what-if" scenarios with the calculator, such as how monthly payments would change if the rate dropped by 0.25%. This enables you to make more informed choices before locking in a rate.

5. As of October 2025, what is the Canadian refinance rate trend?

According to the most recent Bank of Canada report (October 2025), the average rate for a 5-year fixed-term refinance in Canada is currently between 4.6% and 4.9%. As long as inflation stays within the 2–3% target range, rates should remain stable through the end of the year.

6. Is it worthwhile to refinance in 2025?

Yes, refinancing may make sense if your current rate is 1% higher than what's currently available. Following the BoC's July rate cut, many Canadians refinanced this summer, lowering their monthly payments and total loan interest. To be sure, always figure out your break-even point.

People Also Ask

Are Canadian refinance rates declining?

Yes, many lenders started reducing their refinance offers following the BoC's September 2025 cut to 2.50%.

Does my credit score change if I use a refinance calculator?

No, it doesn't. Since online calculators are merely financial simulations, using them is entirely safe. Only when you formally apply for refinance—which results in a hard credit inquiry—does your credit score change.

What distinguishes the "mortgage rate" from the "refi interest rate"?

The rate you receive when you refinance an existing home loan is known as the "refi interest rate." For purchases or refinances, a "mortgage rate" is more generic. Although their contexts differ, they both employ the same pricing logic.

Limitations & Things to Watch

- The calculator doesn’t know lender spreads, credit risk, or future macro changes.

- Penalties may be undervalued.

- It won't take into account mid-term changes to variable rates.

- Always use it as a guide, never use it as the final word

Want to see your own numbers? Try the Rateswise refinance calculator now.

Disclaimer

This content is for educational use only, not legal or financial advice. Lender policies, terms, and rates are subject to frequent changes. Before taking any action, always confirm actual figures with certified mortgage experts or your lenders.

About the Author

Written by the Rateswise Mortgage Team.

We’ll help you understand how to use a calculator and assess actual market data. We have assisted numerous homeowners in Ontario with the refinance process. To help you make decisions, we provide you with clarity, not hype.