Cash-Out Refinance in Ontario & Canada: How to Access Home Equity Wisely

September 15, 2025

Updated: August 2025

Let's keep it simple and learn how a cash-out refinance works. A cash-out refinance in Canada lets Ontario home owners borrow funds. You can use that money for various purposes, such as investing, paying off debt, or even making improvements. In August 2025, refinance interest rates hovered about 4.5% at several brokerages, according to NerdWallet. Explore the rates timely. According to the Bank of Canada, the five-year fixed rate was 6.09% as of August 2025, but some brokerages were offering refinance rates at 4.5% in Canada.

The policy rate set by the Bank of Canada is 2.75% as of August 2025. Although this affects prime lending rates, the rate you see on a mortgage is different.

Let's review how it works, determine if it's a good fit for you in Ontario, and explore how Rateswise can assist you with all of this. Calculate your mortgage refinance rates or get an estimate if you want to refinance. Contact Rateswise team today.

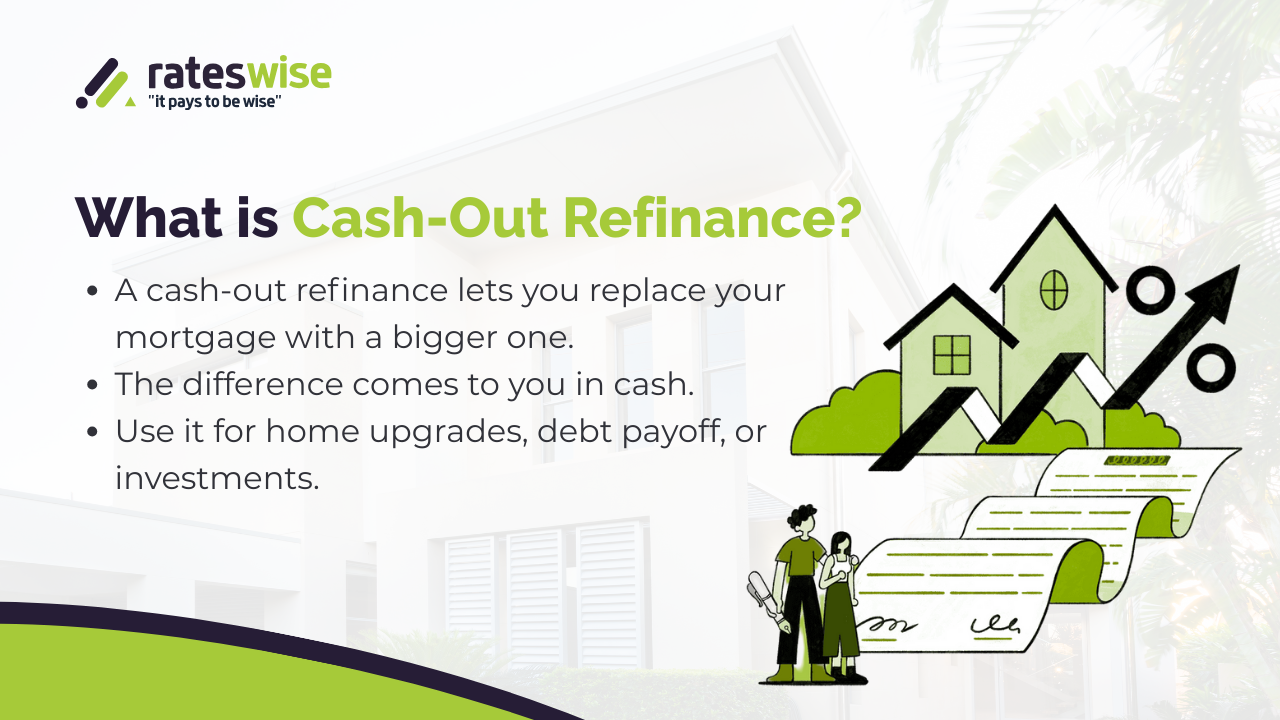

What Is a Cash-Out Refinance?

A cash-out refinance substitutes a larger mortgage for your existing one. The excess funds become cash in your hands.

For example:

- If your home value is $600,000,

- Your mortgage would be $300,000,

- The maximum amount that you can refinance is (80% LTV) $480,000, and

- You get $180,000 in cash after you clear your debt (existing/old mortgage).

How It Works in Canada (specifically Ontario)

- Request a new mortgage from lenders.

- Lenders look at your expenses, income, and credit.

- An appraisal determines the value of your home.

- You pay off your previous mortgage with the new one and take cash with you.

- Over time, you pay back the larger, new mortgage.

Benefits of a Cash-Out Refinance

- Usually have lower interest rates than any credit cards or personal loans. Since lenders use your home as collateral for these loans, rates are frequently significantly cheaper.

- A substantial one-time payment, typically hundreds of thousands of dollars, is spent.

- For lower interest rates, pay off high-interest debt, such as credit cards or credit lines.

- Make improvements to your house that will increase its worth.

Is the Ontario Market in 2025 Smart?

Yes, if properly executed. This might outperform credit card rates, which are typically between 19 and 29 percent, since Canadian refinance rates stood at 6.09% according to the Bank of Canada, but many brokerages and lenders were offering 4.5%. However, keep in mind that any savings could be reduced by prepayment penalties and expenses (legal, appraisal).

*With a cash-out refinance, you can refinance your auto loan through a mortgage, typically at a reduced interest rate. Don't make a 3-year term into a 20-year one, and make sure you account for longer-term expenses.

Who Is Capable of This? (Requirements in Canada)

- About 20% of your home's equity is required.

- Excellent credit score (~620+).

- evidence of a consistent income and the capacity to pay back.

- The majority permit refinances up to 80% LTV.

Comparison: Alternatives to Cash-Out Refinance

For HELOC:

Up to 65% of the home value is available as revolving credit. Good for flexible, smaller needs

For Second Mortgage:

Lump sum with its own repayment plan.Excellent credit score

For Personal Loan:

Fast but higher interest.

Smart Tips to Get the Best Deal

- Shop around — compare rates and try to find the best deal for you.

- Collaborate with a broker to have access to more lenders.

- Raise your credit score before applying to qualify for better terms.

- Run a mortgage calculator (like ours) to see the results in advance; accounting for penalties and fees helps you avoid any surprises.

Real Experience: How Rateswise Helped

A customer requested money for a new kitchen and had $150k in equity. They discovered a lender via Rateswise that offered a refinance rate of 4.49% with costs of less than $1,000. Compared to a personal loan, they saved thousands of dollars after we guided them through the legal, appraisal, and credit processes.

FAQs

A cash-out refinance: what is it?

It involves taking the difference in cash and refinancing your mortgage for more than you currently owe.

In 2025, is it a good idea in Canada?

Yes—just make sure to include in penalties and fees when rates (~4.5%) are better than alternatives.

What distinguishes HELOC from Cash-Out Refinance?

While HELOC offers flexibility with a variable rate and smaller limitations, cash-out offers a flat sum at a reduced rate.

Can someone with bad credit qualify?

You might, but be prepared for reduced lender options and higher rates.

Use our mortgage refinance calculator, and contact our team to get the best refinancing option.

About the Author

Rateswise Team Member

Rateswise has helped hundreds of people in Ontario refinance wisely, increasing long-term savings, clarity, and trust.

Disclaimer

The information in this article is for educational purposes only. Mortgage rates and lending policies in Canada may change without notice. Always consult with a licensed mortgage expert before making any decision.