Mortgage Penalty Calculator Canada Guide

April 8, 2026

Key points/summary:

- A mortgage penalty is the cost of breaking your mortgage early in Canada.

- Variable mortgages usually charge 3 months’ interest (lower cost).

- Fixed mortgages often use IRD (Interest Rate Differential), which can be much higher.

- Always compare penalty vs total savings before refinancing or switching lenders.

What Is a Mortgage Penalty in Canada?

A mortgage penalty is a fee charged when you end your mortgage before the term is complete. This usually happens when you:

- Refinance for a lower rate

- Sell your home before renewal

- Switch lenders

Lenders charge this penalty because they lose expected interest income.

👉 In simple terms: you’re compensating the lender for breaking the agreement early.

For borrowers, this is not just a technical detail. It directly impacts:

- How much you save when refinancing

- whether switching lenders makes financial sense

- How much equity do you keep when selling

We see many homeowners underestimate these penalties, which leads to poor financial decisions.

How Is Mortgage Penalty Calculated?

Mortgage penalties in Canada are typically calculated using two methods:

1. Three Months' Interest

This is the simpler calculation.

It is usually applied to:

- variable-rate mortgages

- Some fixed mortgages with specific conditions

The formula is based on:

👉 remaining mortgage balance × interest rate ÷ 4

Example:

- Balance: $400,000

- Rate: 5%

Penalty ≈ $5,000

Best for: Variable-rate mortgagesKey benefit: Easy to estimate and usually lower

2. Interest Rate Differential (IRD)

This is more complex and often higher.

It is commonly applied to:

- fixed-rate mortgages

The IRD calculation considers:

- Your current mortgage rate

- The lender’s current rate for a similar term

- Remaining time left on your mortgage

Insight: IRD protects the lender’s lost interest—not just a simple fee.

Why Use a Mortgage Penalty Calculator?

Estimating your penalty manually is difficult because:

- Lender formulas vary

- Rates change over time

- Contract terms differ

A mortgage penalty calculator simplifies this by giving you a rough estimate based on:

- your balance

- your rate

- your remaining term

Think of it as your starting point, not the final number.

When Should You Use a Mortgage Penalty Calculator?

You should estimate your penalty before:

- Refinancing for a lower rate

- Switching lenders

- Selling your property early

- Consolidating debt into your mortgage

The key rule:

The decision to break a mortgage should always be based on net financial impact, not just interest savings.

Example

If your penalty is:

- $12,000

and your savings from refinancing

- $8,000

👉 You are actually losing money

This is why calculating the penalty is essential before taking action.

If you are considering refinancing or breaking your mortgage, the first step is understanding your penalty exposure.

We help homeowners evaluate:

- penalty costs

- refinance savings

- net financial outcomes

so they can make informed decisions instead of costly assumptions.

Do Fixed and Variable Mortgages Have Different Penalties?

Yes, fixed and variable mortgages in Canada have very different penalty structures, and this difference can significantly impact your decision.

In most cases:

- Variable-rate mortgages → lower, simpler penalties

- Fixed-rate mortgages → higher, more complex penalties

Understanding this difference is critical before using any mortgage penalty calculator.

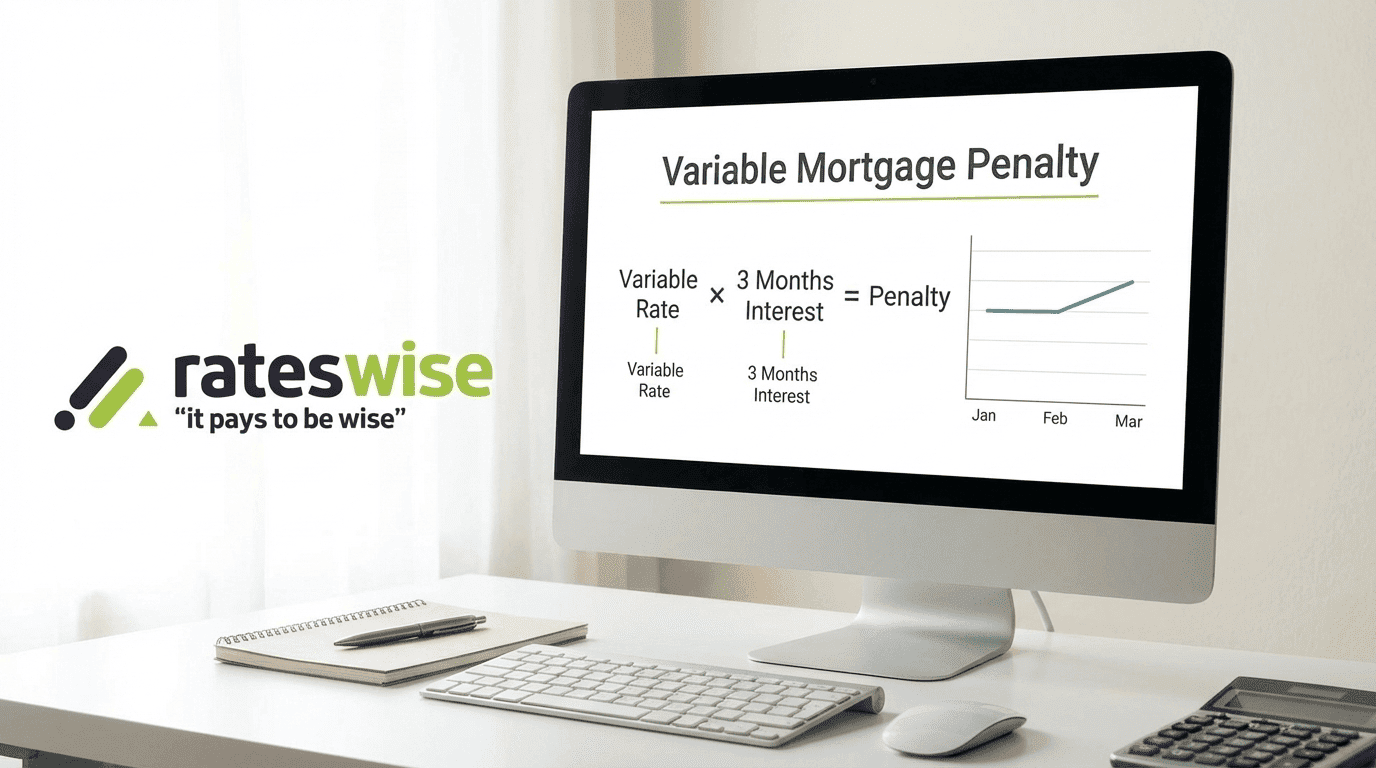

Variable Mortgage Penalty

For most variable-rate mortgages, the penalty is

👉 Three months’ interest

This is calculated based on:

- Your remaining mortgage balance

- Your current interest rate

Example

If you have:

- $400,000 remaining balance

- 5% interest rate

Your penalty would roughly be:

👉 $400,000 × 5% ÷ 4 = $5,000

👉 Insight: Variable mortgage penalties are predictable and usually manageable.

Fixed Mortgage Penalty

Fixed-rate mortgages often use the Interest Rate Differential (IRD) method.

This is where many homeowners are surprised, because IRD penalties can be significantly higher.

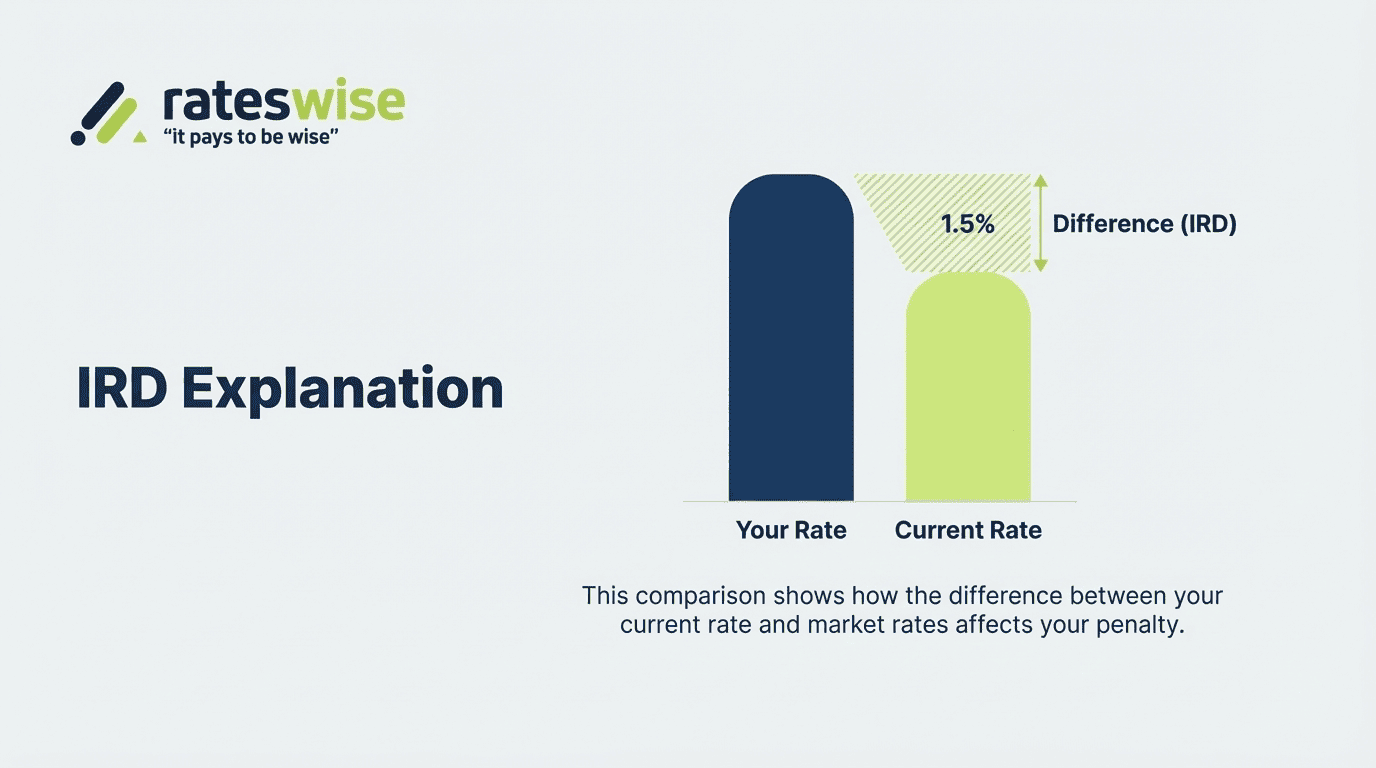

What Is IRD (Interest Rate Differential)?

IRD measures the difference between:

- Your current mortgage rate

- The lender’s current rate for a similar remaining term

Then it applies that difference to your remaining balance over the remaining term.

Why IRD Can Be High

IRD penalties increase when:

- Your original rate is higher than the current market rates

- You have a large balance

- You have a longer time remaining

This is common in markets like Toronto, Vancouver, and Calgary, where rate cycles shift quickly.

Example

You have:

- mortgage rate: 5.5%

- current comparable rate: 3.5%

- difference: 2%

That 2% difference is applied to your remaining balance and term.

👉 This can easily result in penalties of $10,000 to $30,000+, depending on the mortgage size and time remaining.

👉 Insight: IRD is designed to protect the lender’s lost interest, not just charge a simple fee.

Why Mortgage Penalty Calculators Are Important for Fixed Mortgages

Unlike variable penalties, IRD calculations are:

- not standardized across lenders,

- influenced by internal rate sheets,

- affected by timing, and remaining term

This makes manual estimation difficult.

A calculator gives you:

- a realistic estimate

- a starting point for decision-making

- clarity before contacting your lender

Common Mistakes Homeowners Make

Many borrowers:

- Assume all penalties are small

- Refinance without calculating the penalty

- Compare rates, but ignore the total cost

- Not checking lender-specific IRD calculations

👉 Insight: A lower rate does not always mean a better deal.

When Breaking Your Mortgage Actually Makes Sense

Even with a penalty, breaking your mortgage can still be beneficial if:

- Interest savings exceed the penalty

- You are consolidating high-interest debt

- You are restructuring your financial plan

Quick Decision Framework

Before breaking your mortgage, ask:

- What is my estimated penalty?

- How much will I save after refinancing?

- What is my net financial outcome?

👉 Insight: The right decision is based on total cost, not just rate comparison.

If you are unsure how your mortgage penalty affects your refinancing decision, estimating it accurately is the first step.

We help homeowners:

- Calculate realistic penalty estimates

- Compare refinancing scenarios

- Understand the true financial impact

so they can make confident mortgage decisions.

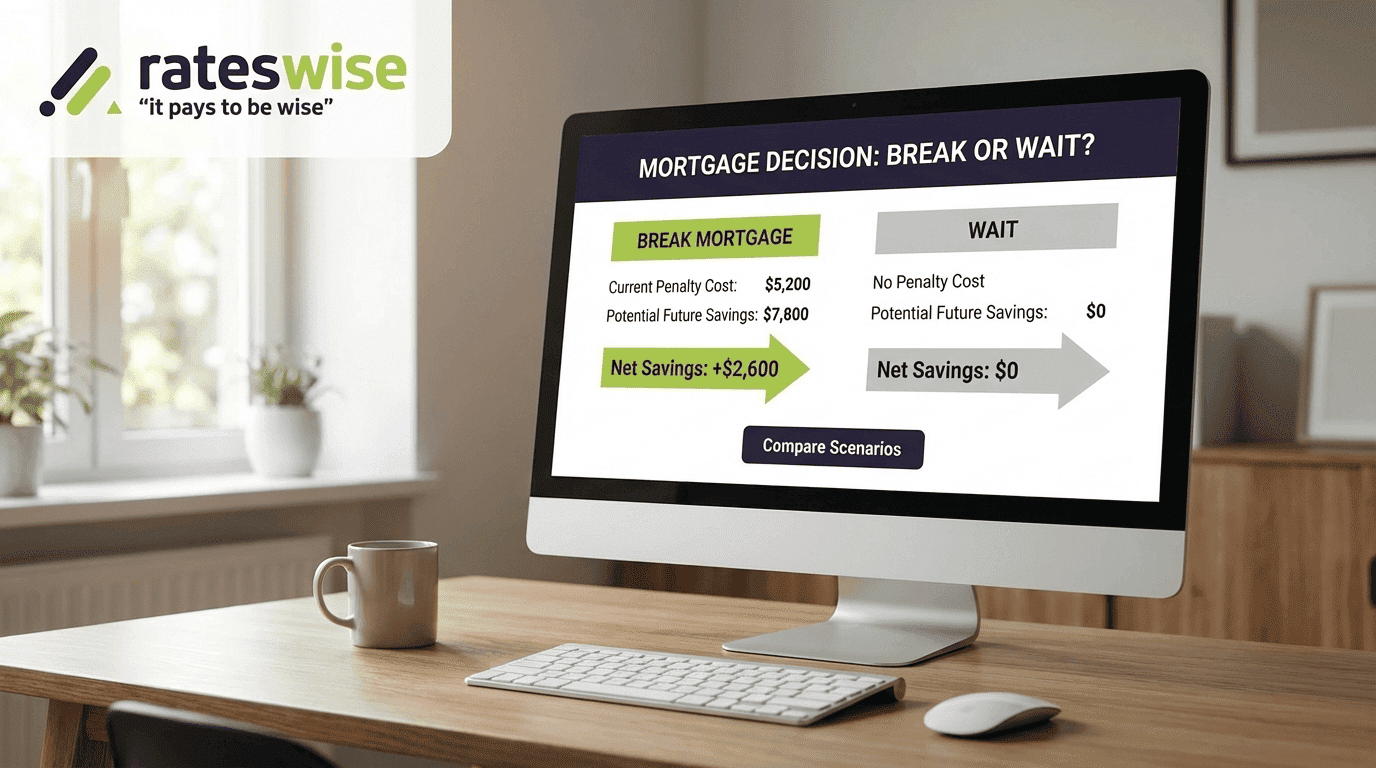

Should You Break Your Mortgage or Wait?

A mortgage penalty calculator gives you a number. But the real decision is whether breaking your mortgage is financially justified.

In many cases, the wrong decision is not about the penalty itself. It is about ignoring the total financial outcome.

When You Should NOT Break Your Mortgage

Avoid breaking if:

1. Small Rate Difference

- Savings are minimal

2. Near Renewal

- Limited time to recover the penalty

3. High IRD Penalty

- Costs outweigh benefits

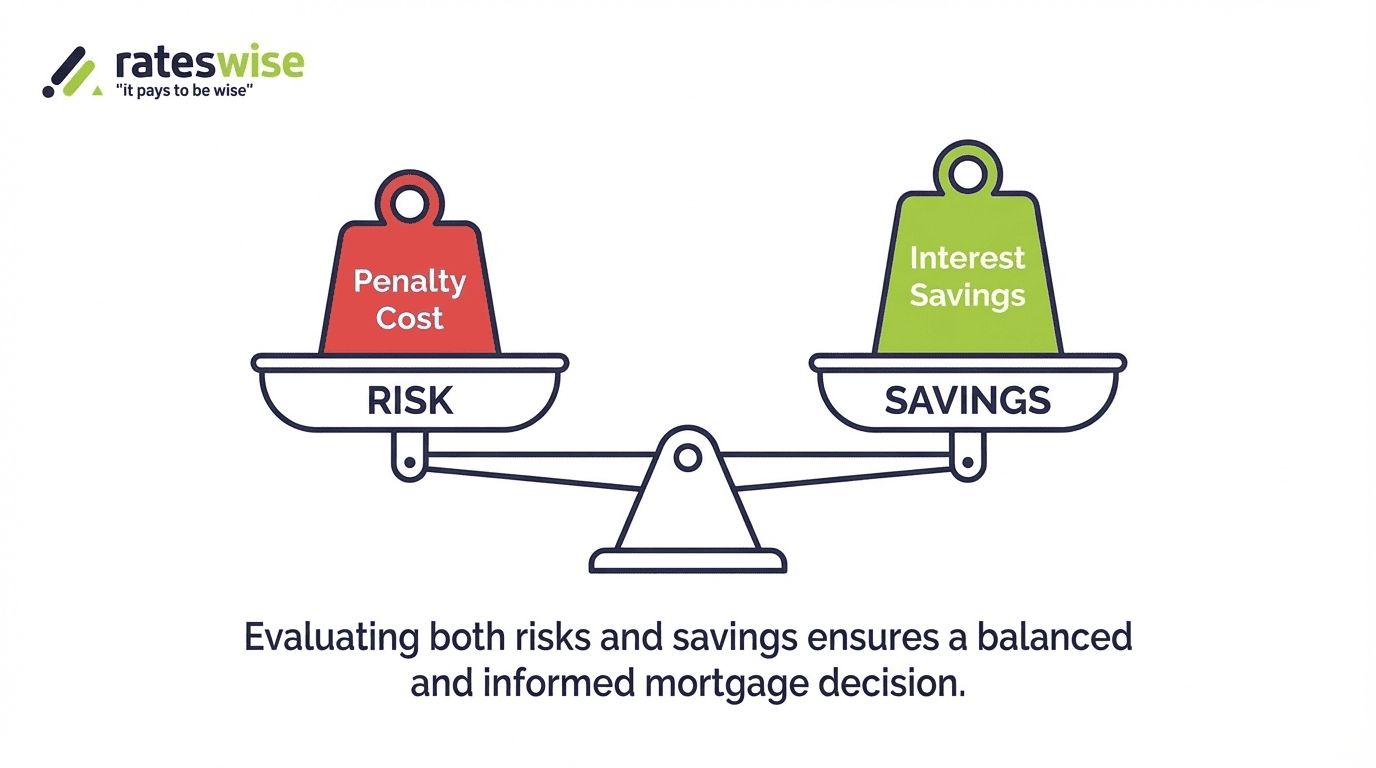

Risk vs Reward Breakdown

When evaluating your decision, consider:

Potential Benefits

- Lower monthly payments

- Reduced interest cost

- Improved cash flow

Potential Risks

- high upfront penalty

- incorrect savings assumptions

- unexpected fees

👉 Insight: The best decisions are based on full cost comparison, not assumptions.

Smart Mortgage Strategy (Canada 2026)

A well-informed borrower does not just:

- check rates

- calculate penalties

They evaluate:

- Penalty calculation

- Rate comparison

- Full cost analysis

- Long-term financial planning

👉 Mortgage decisions should be strategic, not reactive.

Final Thoughts

A mortgage penalty calculator is a powerful tool, but it is only the starting point.

It helps you understand:

- your potential cost

- your financial goals

- your long-term savings

The real value comes from combining that estimate with a structured analysis of your situation.

If you are considering breaking your mortgage, the most important step is understanding the full financial impact, not just the penalty.

At Rateswise, we help homeowners:

- Calculate realistic penalty scenarios

- Compare refinancing options

- Evaluate net savings and risks

This allows you to make confident decisions backed by data, not assumptions.

Frequently Asked Questions

How accurate is a mortgage penalty calculator?

It provides an estimate. The exact penalty depends on your lender’s formula and contract terms.

Are fixed mortgage penalties always higher?

In most cases, yes. Fixed mortgages often use IRD, which can result in higher penalties than variable options.

Can I avoid a mortgage penalty completely?

In some cases, strategies like porting or waiting until renewal can help reduce or avoid penalties.

Does refinancing always save money?

No. You must compare savings against penalties and fees to determine the net outcome.

What is the biggest mistake homeowners make?

Focusing only on lower rates without calculating the total cost.