How to Get Approved for a Mortgage in Canada in 2026

How Do You Increase Your Chances of Mortgage Approval in Canada in 2026?

Getting approved for a mortgage in Canada in 2026 depends less on luck and more on how well you prepare. Lenders are not just evaluating your income. They are assessing your overall financial stability, risk level, and ability to manage long-term debt.

In simple terms:

👉 Mortgage approval is a financial qualification process, not just a formality.

At RatesWise, we see this often: buyers start house hunting first, but approval should come before that. Your financing determines what you can realistically afford.

This guide explains how approval works and what you should focus on before applying.

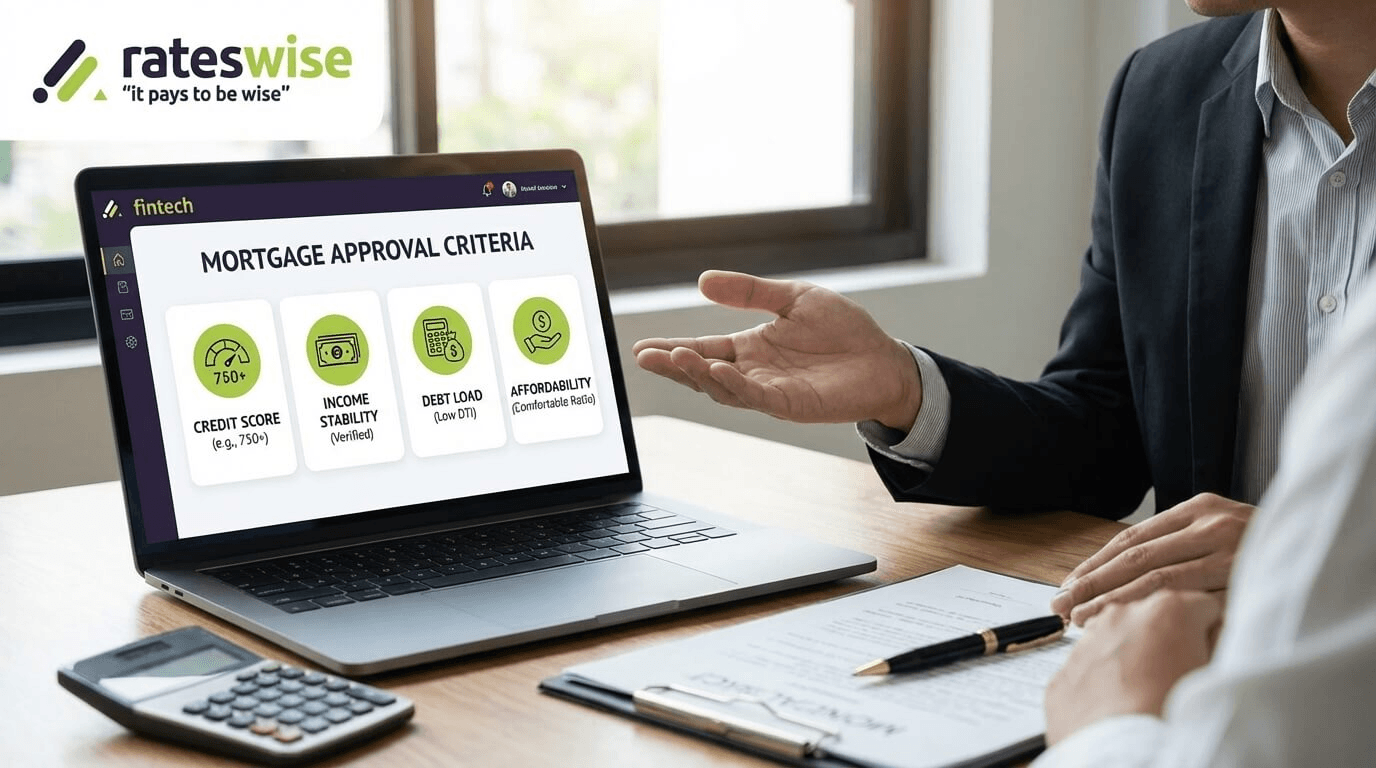

What Do Lenders Actually Look At When Approving a Mortgage?

Mortgage approval is based on your overall financial profile.

Lenders typically assess:

- your credit profile

- your income stability

- your existing debt

- your down payment

- your overall affordability

These factors determine:

- how much you can borrow

- what interest rate you may receive

- how much risk you represent

👉 Insight: Approval is not just about income. It is about financial consistency.

Why Preparation Matters More Than Timing

Many borrowers assume the application is the most important step.

In reality, the preparation phase determines the outcome.

If your financial profile is:

- well-structured

- stable

- clearly documented

your chances of approval improve significantly.

On the other hand, applying without preparation can lead to:

- lower approved amounts

- higher interest rates

- potential rejection

👉 Insight: The strongest applications are built before they are submitted.

The First Step Most Buyers Overlook

Know Your Financial Position

Before applying, you need clarity on where you stand financially.

This includes:

- knowing your credit score

- understanding your monthly obligations

- evaluating your savings and liquidity

Without this, you’re guessing how lenders will evaluate you.

Why Approval Comes Before Home Search

Many buyers start with property searches, listings, and open houses.

However:

👉 the ability to secure financing determines what you can realistically purchase

Without approval clarity:

- your budget is uncertain

- your negotiation position is weaker

- your buying process becomes reactive

This is why mortgage approval is considered one of the most critical steps in the home-buying process.

What This Means for Buyers in 2026

In today’s Canadian market, lenders expect:

- Stable income

- Controlled debt

- Long-term affordability planning

With higher borrowing costs and stricter assessments, preparation is more important than ever.

Insight

Mortgage approval is not something you try.

It is something you prepare for deliberately.

If you are planning to buy a home and are unsure where you stand financially, the first step is not applying, it is understanding your approval readiness.

At Rateswise, we help buyers break down their financial position and identify what needs to be improved before submitting a mortgage application.

How Do Credit Score and Down Payment Affect Mortgage Approval?

Your credit score and down payment are two of the most influential factors in mortgage approval. They directly impact :

- your approval chances

- your borrowing limit

- your interest rate

Why Your Credit Score Matters More Than You Think

In Canada, credit scores range from 300–900.

- 660+ → generally qualifies for better options

- Higher scores → better rates and flexibility

A strong score shows:

- On-time payments

- Low credit usage

- Consistent financial behavior

👉 Even a small improvement can reduce your borrowing cost.

How to improve it:

- Pay bills on time

- Reduce credit card balances

- Avoid new credit before applying

Down Payment: Why It Matters

Your down payment reduces lender risk.

Minimum requirements in Canada:

- Under $500K → 5%

- $500K–$1.5M → 5% + 10% on remaining

- Over $1.5M → 20%

A larger down payment:

- Lowers monthly payments

- Improves affordability

- Increases approval confidence

Bigger down payment = stronger application.

How to Improve Your Credit Position Before Applying

If your score is not where it should be, small adjustments can help:

- make all payments on time

- reduce credit card balances

- avoid new credit applications before applying

Improving your score even slightly can strengthen your overall application.

Mortgage Insurance (Important in Canada)

If your down payment is under 20%, mortgage insurance is required.

- Adds to your loan cost

- Increases monthly payments

- May qualify you for slightly better rates (lower lender risk)

How Credit and Down Payment Work Together

Credit score and down payment are not evaluated separately.

They work together to shape your application strength.

For example:

- strong credit + low down payment → moderate approval strength

- average credit + large down payment → improved risk profile

- strong credit + large down payment → best positioning

keypoint:

Improving either your credit score or your down payment helps.

Improving both creates a significantly stronger application.

If you are unsure whether your credit profile or down payment is strong enough, evaluating both before applying can prevent costly mistakes.

At Rateswise, we help buyers:

- understand how lenders will assess their profile

- identify gaps that may affect approval

- create a structured plan before applying

This approach allows you to apply with clarity instead of uncertainty.

How Do Income Stability and Existing Debt Impact Mortgage Approval?

Your income and existing debt play a critical role in mortgage approval because they determine whether you can realistically handle long-term payments.

Lenders are not only asking:

👉 how much you earn

They are also asking:

how stable your income is

how much of it is already committed

Why Stable Income Is a Key Approval Factor

Lenders prefer borrowers with predictable and consistent income.

This is because mortgage payments are long-term obligations, and lenders want confidence that you will continue earning over time.

What Lenders Look for in Income

Typically, lenders evaluate:

- employment type (full-time, part-time, self-employed)

- length of employment

- income consistency over time

Stable employment signals lower risk.

Why Job Changes Can Affect Approval

Changing jobs during the mortgage process can create uncertainty.

Even if your income remains similar, lenders may view:

- probation periods

- short employment history

- inconsistent earnings

as higher risk.

Insight: Stability often matters more than short-term income increases.

Special Case: Self-Employed Borrowers

If you are self-employed, approval requirements are usually stricter.

Lenders may ask for:

- multiple years of income history

- proof of business stability

- financial documentation

This is because income may fluctuate more compared to salaried roles.

How Existing Debt Affects Your Mortgage Approval

Debt is one of the most overlooked factors by borrowers.

Lenders evaluate your debt-to-income ratio, which measures how much of your income is already committed to existing obligations.

Common Types of Debt Considered

- credit card balances

- personal loans

- student loans

- lines of credit

These do not need to be fully paid off, but they must be manageable.

Why Debt Reduces Borrowing Power

Higher debt levels:

- reduce the amount you can borrow

- increase your risk profile

- may lead to higher interest rates

👉 Insight: Even moderate debt can significantly impact approval outcomes.

The Goal Is Not Zero Debt, It Is Controlled Debt

You do not need to eliminate all debt before applying.

However, lenders expect:

- reasonable balances

- consistent repayment history

- manageable monthly obligations

Income + Debt = Real Approval Strength

Lenders do not evaluate income and debt separately.

They look at how they interact.

For example:

- high income + high debt → reduced affordability

- moderate income + low debt → stronger profile

👉 Insight: Approval strength depends on balance, not just income level.

Why Mortgage Pre-Approval Is a Smart Step

A mortgage pre-approval gives you a clearer picture of your position before you start house hunting.

It includes:

- estimated borrowing amount

- indicative interest rate

- preliminary lender assessment

Pre-approvals are often valid for a limited time, allowing you to search for a home with more confidence.

Benefits of Getting Pre-Approved

- understand your realistic budget

- identify potential issues early

- strengthen your position when making offers

Remember

Income stability and debt management are two of the strongest signals lenders use.

A well-balanced financial profile is more effective than simply having a high income.

If you are not sure how your income and existing debt will affect your approval, reviewing your financial structure before applying can make a significant difference.

At Rateswise, we help buyers:

- assess their income stability from a lender perspective

- understand how debt impacts borrowing capacity

- prepare for pre-approval with clarity

This allows you to move forward with a stronger and more structured application.

How Do You Secure a Better Mortgage Rate in 2026?

Getting approved for a mortgage is one part of the process. Securing a competitive rate is what determines how much you actually pay over time.

A lower interest rate can:

- reduce your monthly payment

- lower total interest cost

- improve long-term affordability

However, rates are not fixed across all lenders. They vary based on your financial profile and how you approach the process.

Why Rate Shopping Matters More Than Most Buyers Realize

Many borrowers accept the first rate they are offered.

This is a mistake.

Different lenders assess risk differently, which means:

- the same borrower can receive different rates

- small differences in rate can lead to large cost differences over time

👉 Insight: Mortgage rates are negotiable within a range, not fixed for every borrower.

How to Approach Rate Comparison Strategically

Instead of focusing on a single offer, compare multiple options.

This can include:

- different lenders

- different mortgage structures

- different terms

Using structured comparison tools or working with a mortgage expert can help identify better options.

Why a Better Rate Improves Approval Strength

A lower rate does more than reduce cost.

It also improves:

- affordability calculations

- debt ratios

- overall approval likelihood

This means that finding a better rate can indirectly strengthen your application.

Understanding What You Can Actually Afford

One of the most important steps is defining a realistic budget.

Lenders will approve you based on formulas, but those formulas do not account for your full lifestyle.

You need to consider:

- monthly living expenses

- future financial plans

- unexpected costs

👉 Insight: Approval amount is not the same as affordability.

Hidden Costs in Canada

Many buyers overlook:

- Property taxes

- Utilities

- Maintenance

- Closing costs (often 1.5%–4%)

👉 Ignoring these leads to financial pressure after purchase.

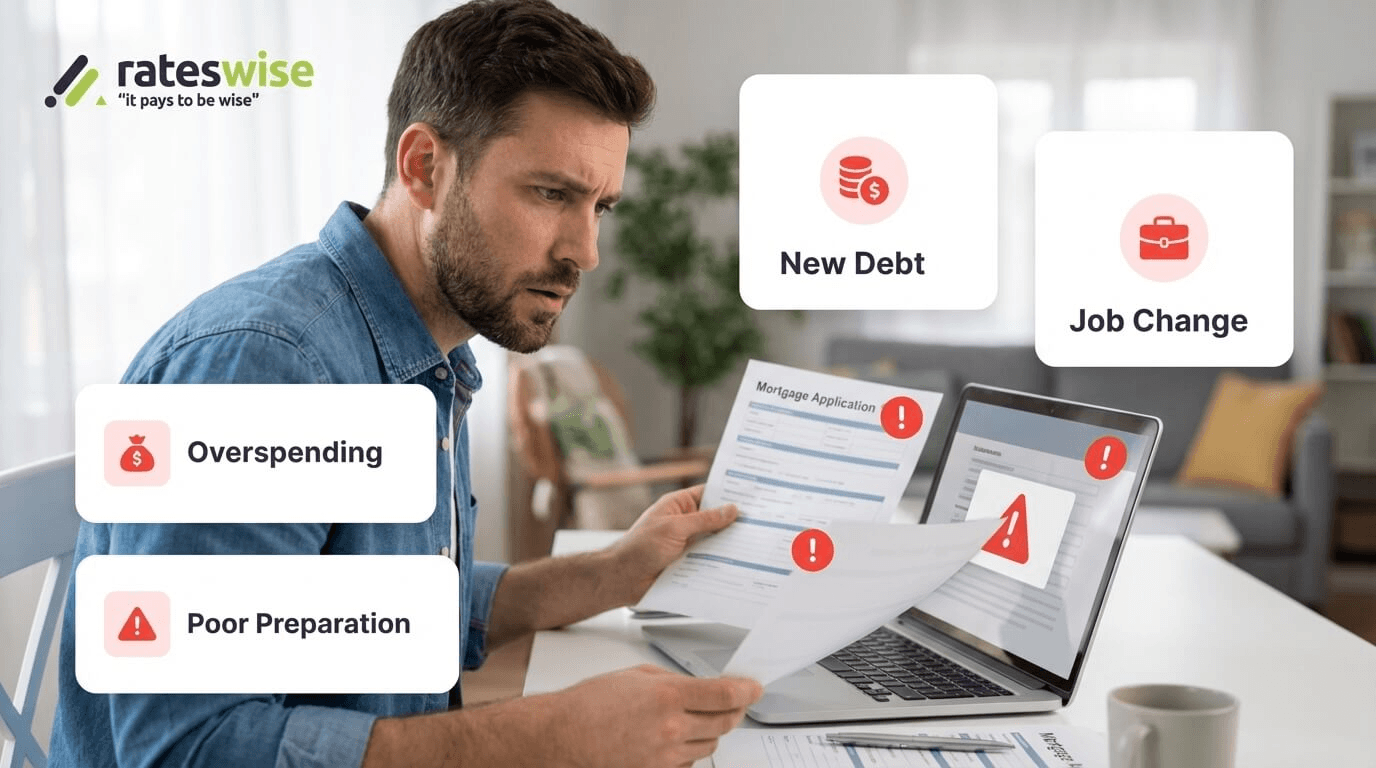

Common Mistakes To Avoid

Even strong applicants can weaken their profile by making avoidable mistakes.

Applying Without Preparation

Submitting an application without reviewing your financial profile can lead to poor results.

Taking on New Debt Before Approval

New loans or increased credit balances can reduce your borrowing capacity.

Changing Jobs During the Process

Unstable income signals higher risk to lenders.

Overestimating Affordability

Buying at the maximum approved level can create long-term financial strain.

Keypoint

Mortgage approval and rate selection are connected.

The strongest outcomes come from:

- preparing your financial profile

- understanding your affordability

- comparing options carefully

Final Thoughts

Getting approved for a mortgage in 2026 is not about meeting minimum requirements. It is about presenting a strong, stable, and well-prepared financial profile.

The better your preparation:

- the higher your approval chances

- the better your rate options

- the more control you have over your purchase

If you are planning to apply for a mortgage and want to improve both your approval chances and your rate options, the first step is understanding how lenders will evaluate your profile.

We help

- identify weaknesses before applying

- compare realistic rate options

- build a structured mortgage strategy

This allows you to move forward with clarity instead of guesswork.

Frequently Asked Questions

What is the most important factor in mortgage approval?

There is no single factor. Lenders evaluate credit, income, debt, and down payment together.

Can I improve my approval chances quickly?

Yes. Small changes such as reducing debt or improving credit usage can make a noticeable difference.

Should I focus more on rate or approval?

Both matter. Approval determines access, while the rate determines cost.

Is pre-approval necessary?

It is not mandatory, but it provides clarity and strengthens your buying position.

How do I know what I can truly afford?

You need to evaluate your full financial situation, not just lender calculations.

Disclaimer

This information is intended only as general guidance. Lender rules, margins, and rates are subject to change. Always confirm current figures and consult a qualified mortgage expert before refinancing.