Fixed vs Variable Mortgage Canada 2026 Guide

April 1, 2026

Fixed vs Variable Mortgage in Canada in 2026: Whichis Better Option Right Now?

In 2026, the choosing between a fixed and variable mortgage in Canada depends largely on your risk tolerance, cash-flow needs, and expectations for interest rates.

As of March 2026, the Bank of Canada has held its policy rate at 2.25%, which helps anchor variable-rate pricing, while widely advertised market rates show roughly 3.99% for a five-year fixed and around 3.35% for a five-year variable for some insured buyers.

Variable rates are often lower today. However, a lower rate does not always mean lower total cost over time.

This guide explains how fixed and variable mortgages work, how rates affect each option, and what borrowers should evaluate before locking into either structure.

What Is the Difference Between a Fixed and Variable Mortgage?

A fixed mortgage is better if you want stable payments and protection from rising rates.

A variable mortgage may be better if you want a lower starting rate and can handle changes in interest costs.

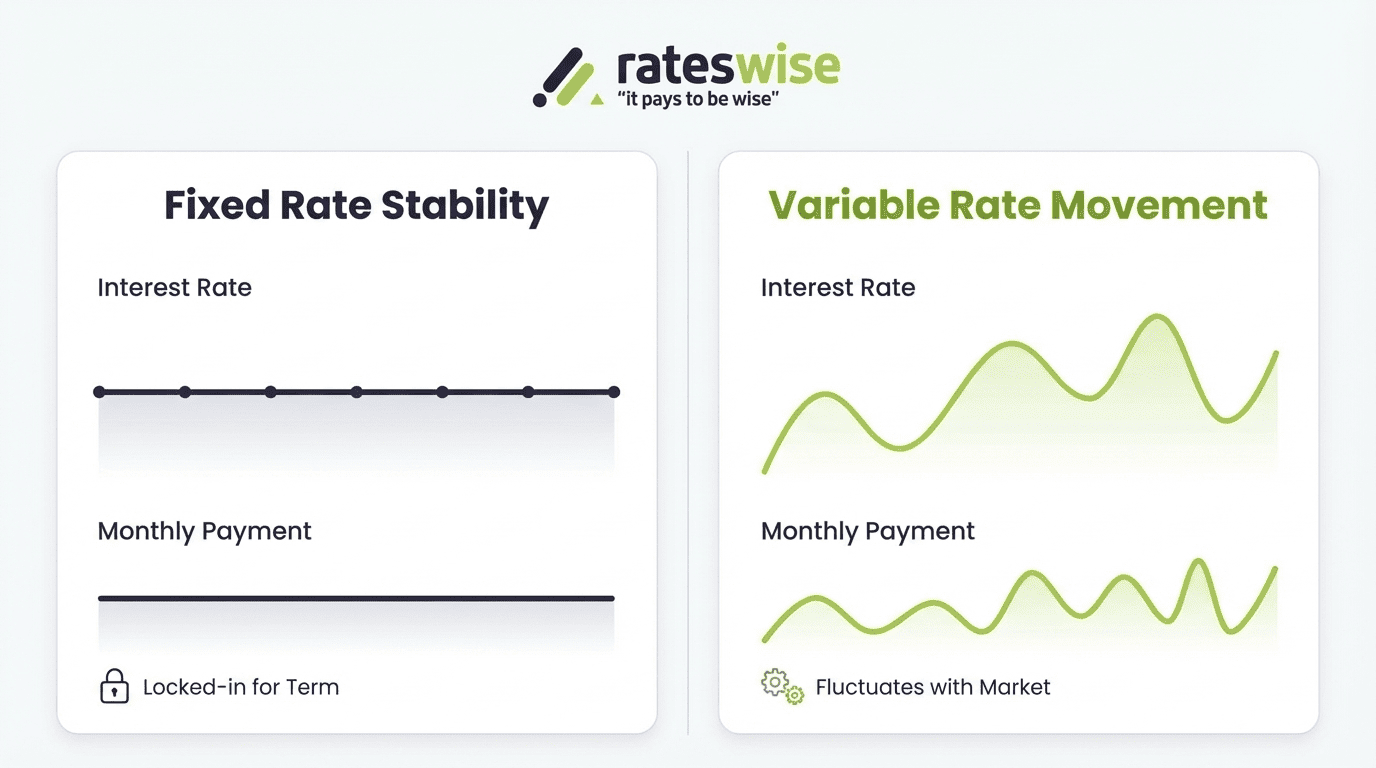

A fixed mortgage has an interest rate that stays the same for the entire term. Your payment structure is predictable even if market rates increase.

A variable mortgage has an interest rate that changes based on the lender’s prime rates, which are influenced by the Bank of Canada’s policy rate. When the central bank changes its benchmark, lenders often adjust prime accordingly, and variable-rate borrowers may see changes in interest cost.

In simple terms:

- fixed = stability and predictability

- variable = lower initial rate potential, but more uncertainty

Why This Decision Matters More in 2026

This is not just a pricing question. It is a budgeting decision.

Borrowers today are entering the market after a period of higher interest rates compared to previous years. At the same time, rates have recently stabilized.

This creates a key decision:

👉 Should you choose a lower rate today, or protect yourself from future rate changes?

That is the real difference between fixed and variable mortgages in 2026.

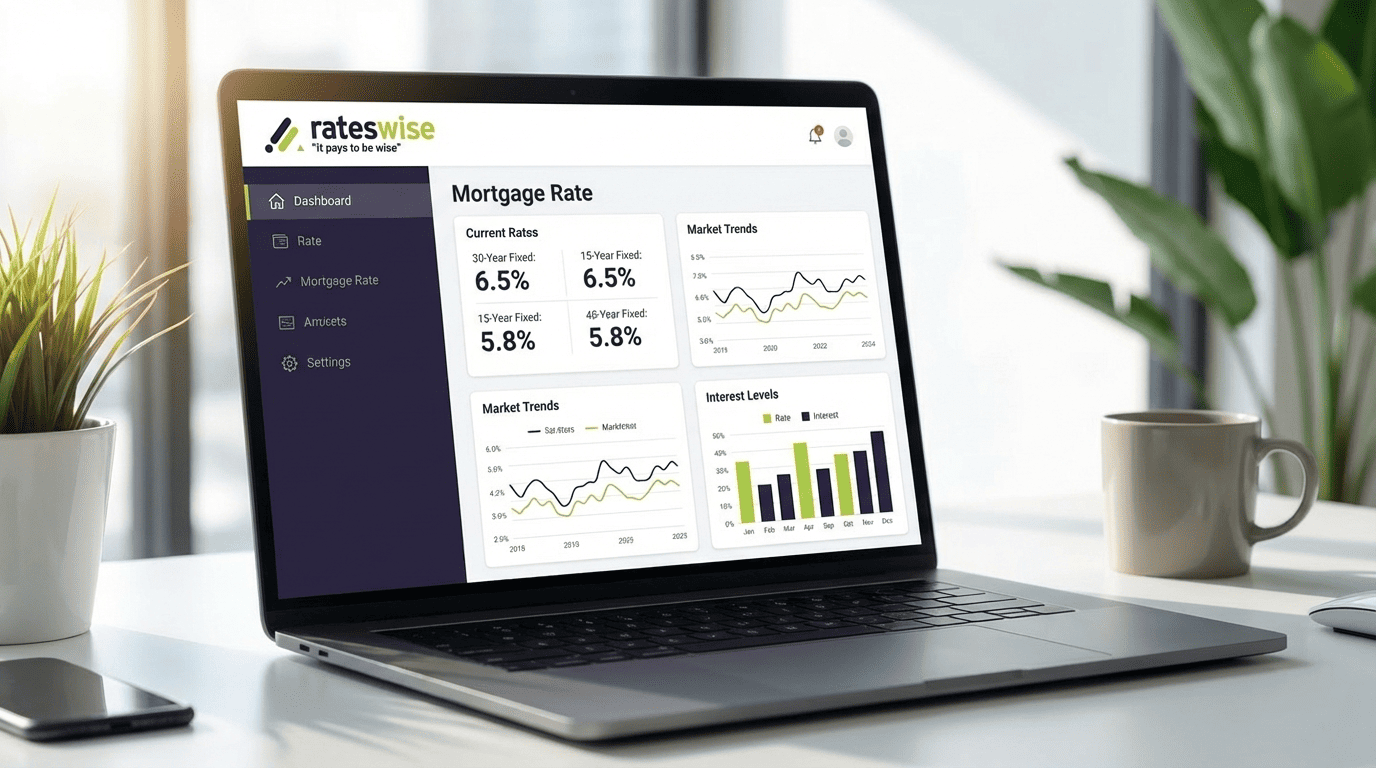

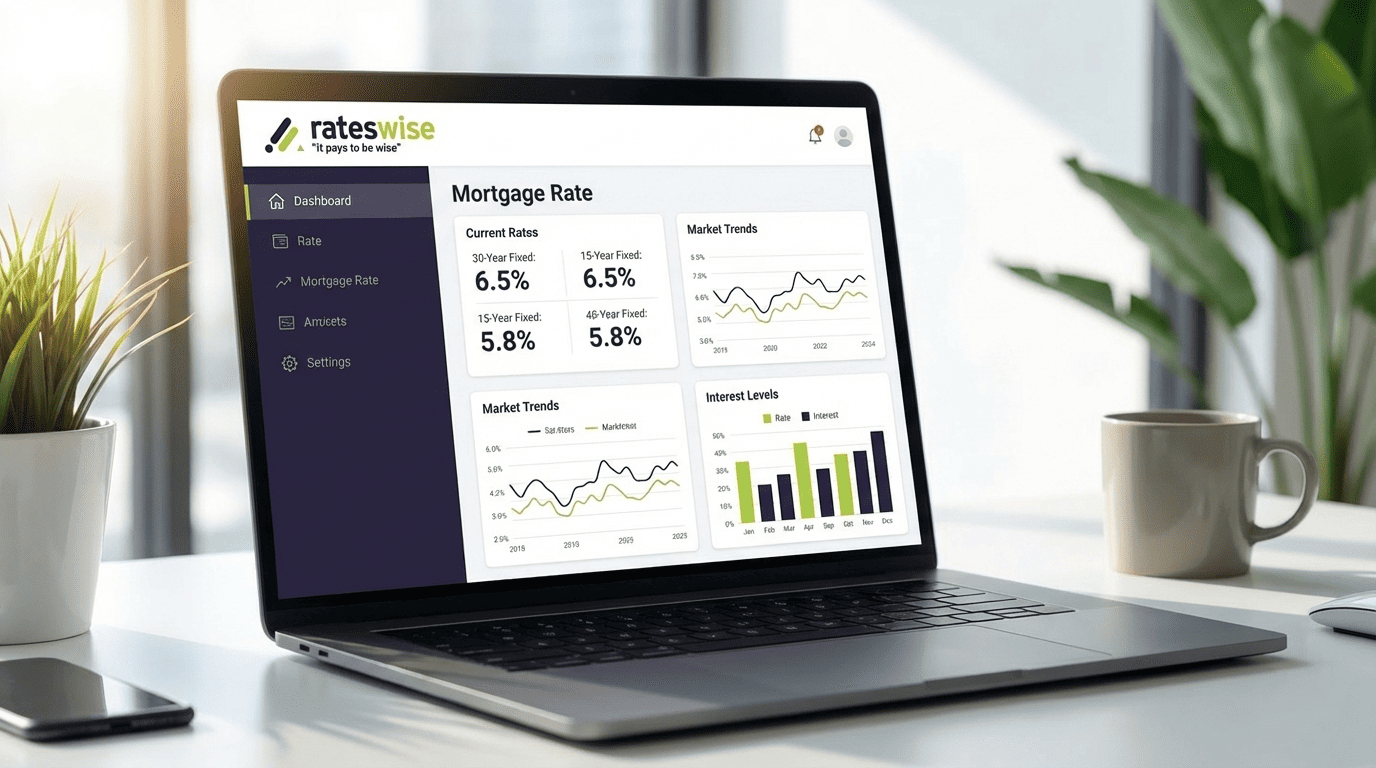

Where Mortgage Rates Stand Right Now

As of March 27, 2026, Ratehub reported:

- 5-year fixed mortgage: ~3.99%

- 5-year variable mortgage: ~3.35%

- Bank of Canada policy rate: ~2.25%

This matters because variable mortgages are influenced by the central bank decisions, while fixed mortgages are influenced more by bond-market expectations and lender pricing strategy.

Why a Lower Variable Rate Is Not Always Better

A variable mortgage may start with a lower rate, but that advantage only lasts if rates remain stable or decline.

If rates rise, increases:

- Interest cost may increase

- More payments go toward interest

- Budgeting becomes harder

A fixed mortgage usually starts higher, but it offers clarity. You know your rate environment from day one.

👉 Key Insight: Lower today does not guarantee lower over time.

Strategic Takeaway

In 2026, variable mortgages may look cheaper on paper, but fixed mortgages still appeal strongly to borrowers who value certainty.

The better option depends less on headlines and more on how much payment fluctuation your budget can realistically absorb.

What Are the Pros and Cons of Fixed vs Variable Mortgages in 2026?

Choosing between a fixed and variable mortgage is ultimately a trade-off between predictability and flexibility. Each option has clear advantages and limitations depending on your financial situation and how you expect interest rates to behave over time.

Fixed Mortgage: Pros and cons

A fixed mortgage provides consistency. Your interest rate stays the same for the entire term, which means your payments remain stable.

Advantages

Payment Certainty You know exactly how much you will pay each month. This makes budgeting easier, especially for households with fixed incomes or tight margins.

Protection From Rate Increases If market rates rise during your term, your rate remains unchanged. This protects you from unexpected increases in borrowing costs.

Simplified Financial Planning Long-term planning becomes easier because your housing costs are predictable. This is particularly useful for families managing multiple financial commitments.

Limitations

Higher Starting Rate Fixed mortgages often begin at a higher rate than variable options, which increases your initial cost.

Less Flexibility Breaking a fixed mortgage early can result in higher penalties compared to variable options.

No benefit if rates fall If rates decline, you do not automatically benefit unless you refinance, which may involve additional costs.

👉 Insight: Fixed mortgages are designed for stability, not optimization.

Variable Mortgage: Lower Entry Cost With Uncertainty

Variable mortgages are linked to lenders’ prime rates, which are influenced by central bank decisions. This means your rate can change during the term.

Advantages

Lower Initial Rate Variable options often start lower than fixed rates, reducing your initial monthly interest cost.

Potential Savings Over Time If rates remain stable or decline, borrowers may pay less interest over the term compared to fixed-rate options.

Greater Flexibility Variable mortgages typically have lower penalties if you break the term early, which can be beneficial if your plans change.

Limitations

Rate Volatility Your borrowing cost can increase if market rates rise, which may impact your monthly payment or amortization.

Budget Uncertainty Even if payments remain fixed, the interest can increase, slowing down principal repayment.

Emotional Pressure Fluctuating rates can create uncertainty, especially for borrowers who prefer a predictable cost.

👉 Insight: Variable mortgages can be financially efficient, but they require tolerance for change.

Which Option Is Better For You?

The right choice depends on how you manage financial risk.

Fixed Mortgage May Be Better If You:

- prefer stable monthly payments

- want protection from future rate increases

- value long-term predictability

- have limited flexibility in your budget

Variable Mortgage May Be Better If You:

- are comfortable with rate fluctuations

- want a lower starting rate

- expect stable or declining rates

- value flexibility and lower break penalties

Real-World Scenario Comparison

Consider two borrowers with similar financial profiles:

- Borrower A chooses a fixed mortgage for payment stability

- Borrower B chooses a variable mortgage for a lower initial rate

If rates remain stable, lower entry

- Borrower B may save on interest

If rates increase:

- Borrower A benefits from protection

- Borrower B faces higher costs or slower principal reduction

👉 Insight: The better option is not universal. It depends on how your financial situation reacts to changing conditions.

Fixed mortgages reduce uncertainty but may cost more upfront. Variable mortgages can reduce initial costs but introduce potential variability.

The decision is less about predicting the market and more about choosing the structure that aligns with your financial comfort level.

What Should You Expect From Mortgage Rates in 2026?

Mortgage rate direction in 2026 depends on:

inflation, economic growth, and central bank policy decisions.

While exact movements cannot be predicted with certainty, current conditions suggest a more stable rate environment compared to previous years, with gradual adjustments rather than sharp changes.

For borrowers, this creates a different decision dynamic:

👉 Instead of reacting to rapid rate hikes, the focus shifts to risk management and long-term planning

In general:

- stable rates → variable becomes attractive

- falling rates → variable may save money

- rising rates → fixed provides protection

👉 The goal is not to predict rates perfectly. 👉 The goal is to choose a structure that fits your financial situation.

How Rate Trends Affect Fixed vs Variable Choices

Fixed and variable mortgages respond differently to market conditions.

- Fixed rates are influenced by bond markets and long-term expectations

- Variable rates move with lender prime rates, which are tied to central bank decisions

This means:

- fixed rates reflect future expectations

- variable rates reflect current policy direction

If Rates Stay Stable

If rates remain relatively steady:

- Variable borrowers benefit from lower initial pricing

- Fixed borrowers maintain predictability but may pay slightly more

If Rates Gradually Decline

If the environment shifts toward lower rates:

- Variable mortgages may become more cost-efficient

- Fixed borrowers may miss potential savings unless they refinance

If Rates Increase Again

If inflation pressures return and rates rise:

- Fixed borrowers are protected

- variable borrowers face higher costs or slower repayment

👉 Insight: The choice is less about guessing rates and more about preparing for different scenarios.

How to Decide?

Instead of guessing the market, ask:

- Can I handle higher payments if rates rise?

- Do I need stable monthly expenses?

- How long will I keep this mortgage?

- Am I comfortable with financial uncertainty?

Your answers will guide your decision.

Here’s a simple process on how to evaluate your financial profile and make a decision.

Step 1: Evaluate Your Financial Flexibility

Ask:

- Can you handle payment increases if rates rise?

- Do you have room in your budget for fluctuations?

If flexibility is limited, stability becomes more important.

Step 2: Define Your Risk Tolerance

Some borrowers prefer certainty, while others are comfortable with variability.

- low risk tolerance → fixed structure

- higher tolerance → variable may be acceptable

Step 3: Consider Your Time Horizon

Think about how long you expect to keep the mortgage.

- shorter horizon → flexibility may matter more

- longer horizon → stability may provide peace of mind

Step 4: Review Your Overall Financial Goals

Mortgage decisions should align with:

- savings plans

- investment strategies

- lifestyle expenses

The goal is to choose a structure that supports your broader financial plan.

👉 Insight: A mortgage should fit your financial strategy, not just current rates.

Common Mistakes Borrowers Make

Even experienced borrowers often make decisions based on incomplete reasoning.

Focusing Only on the Lowest Rate

A lower rate today does not guarantee a lower total cost over time. Structure matters as much as pricing.

Trying to Time the Market

Predicting exact rate movements is extremely difficult. Decisions based purely on forecasts can lead to unnecessary risk.

Ignoring Personal Financial Limits

Choosing a variable option without considering budget flexibility can create stress if conditions change.

Overlooking Penalty Structures

Breaking a mortgage early can be costly, especially with fixed terms. This should be considered upfront.

A Practical Decision Framework

To simplify the choice, consider:

- Do I prioritize stability or flexibility?

- Can I handle changes in borrowing cost?

- How important is predictable budgeting?

- Am I planning to keep this mortgage long-term?

Your answers will naturally point toward the structure that fits your situation.

Takeaway

There is no universal best mortgage type in 2026.

The right decision comes from aligning:

- your financial stability

- your risk tolerance

- your long-term goals

with the characteristics of each option.

ROI and Risk Snapshot: Fixed vs Variable Mortgages

Choosing between a fixed and variable mortgage is not just about interest rates. It is about understanding the long-term financial impact and risk exposure of each option.

Potential Financial Outcomes

A fixed mortgage offers cost consistency.

- predictable monthly payments

- stable long-term budgeting

- protection from rising rates

This makes it easier to manage household finances, especially over multi-year periods.

A variable mortgage, on the other hand, introduces flexibility.

- lower starting rate

- potential savings if rates remain stable or decline

- adaptability to changing market conditions

However, these benefits depend on how rates behave during the term.

👉 Insight: Fixed mortgages optimize for stability, while variable mortgages optimize for potential cost efficiency.

Risk Comparison

Every mortgage structure carries a different type of risk.

Fixed Mortgage Risk

- You may lock in at a higher rate than future market levels

- Limited ability to benefit if rates decline

- Higher penalties if you exit early

Variable Mortgage Risk

- Exposure to rising rates

- Potential increase in monthly cost or slower principal repayment

- Less certainty in long-term budgeting

👉 Insight: Fixed reduces uncertainty risk. Variability reduces opportunity cost risk.

Final Thoughts

There is no single best mortgage option in 2026.

A fixed mortgage offers stability and protection. A variable mortgage offers flexibility and potential savings.

The right choice depends on how you manage risk, not just current interest rates.

Your financial profile review can help you:

- Understand how different rate scenarios affect your payments

- Evaluate long-term affordability

- Choose a mortgage strategy aligned with your goals

If you are comparing options or planning a purchase, getting a clear breakdown of fixed vs variable scenarios can help you make a more confident decision.

Frequently Asked Questions

Is a fixed mortgage safer than a variable mortgage?

Yes. A fixed mortgage is generally more predictable, as it provides stable payments. This reduces uncertainty but may come at a higher initial cost.

Can variable rates change monthly?

Yes, they change when lenders adjust their prime rate, which is influenced by central bank policy decisions.

Which option is cheaper in the long run?

It depends on how interest rates move during your term. Variable mortgages can be cheaper if rates remain stable or decline, while fixed mortgages protect against rate increases.

Can I switch from variable to fixed later?

Some lenders allow it, but terms depend on market conditions.

What is more important: rate or structure?

Both matter. The structure determines how your mortgage behaves over time, while the rate affects your immediate cost.