How Much Mortgage Can You Afford in Canada (2026)?

March 30, 2026

How Much Mortgage Can You Afford?

- Most lenders allow:

- Up to 39% of your income for housing costs (GDS)

- Up to 44% of your income for total debt (TDS)

- Your affordability depends on:

- Income

- Existing debt

- Interest rates

- Down payment

- A practical rule:

👉 Stay below your maximum approval to avoid financial strain

Mortgages are no longer simple approvals.

Today, affordability is about long-term sustainability, not just qualification.

Mortgage affordability in Canada depends on three primary factors: your income, debt levels, and interest rates. In simple terms, most lenders allow borrowers to spend approximately 39% of gross income on housing costs and up to 44% on total debt obligations, including loans and credit cards.

However, affordability is not just about what a lender approves. It is about what you can realistically sustain over time without financial strain.

This guide explains how affordability works, what influences it, and how to evaluate your buying capacity before committing to a mortgage.

What Does Mortgage Affordability Actually Mean?

Mortgage affordability is the home price you can reasonably purchase based on your financial profile.

It is calculated by the following amounts

- annual household income

- Monthly expenses and debt

- Down payment

- Mortgage interest rates

- Amortization period

Lenders assess these factors to determine whether you can manage monthly payments consistently.

From a practical perspective, affordability is not just a number.

It is the ability to:

- Maintain stable cash flow

- Handle interest rate increases

- Manage unexpected costs

It is not just a number. It is a long-term financial position.

Why Is Mortgage Affordability More Complex Than It Looks?

Many buyers assume income determines affordability. It does not.

Two people with the same salary can qualify for very different mortgage amounts.

For example:

- A borrower with no debt can qualify for a higher loan

- A borrower with an existing loan will qualify for less

Lenders apply a stress test, meaning you must qualify at a higher rate than your actual mortgage rate.

- This protects both you and the lender from future rate increases.

How does interest rate impact mortgage affordability or buying power?

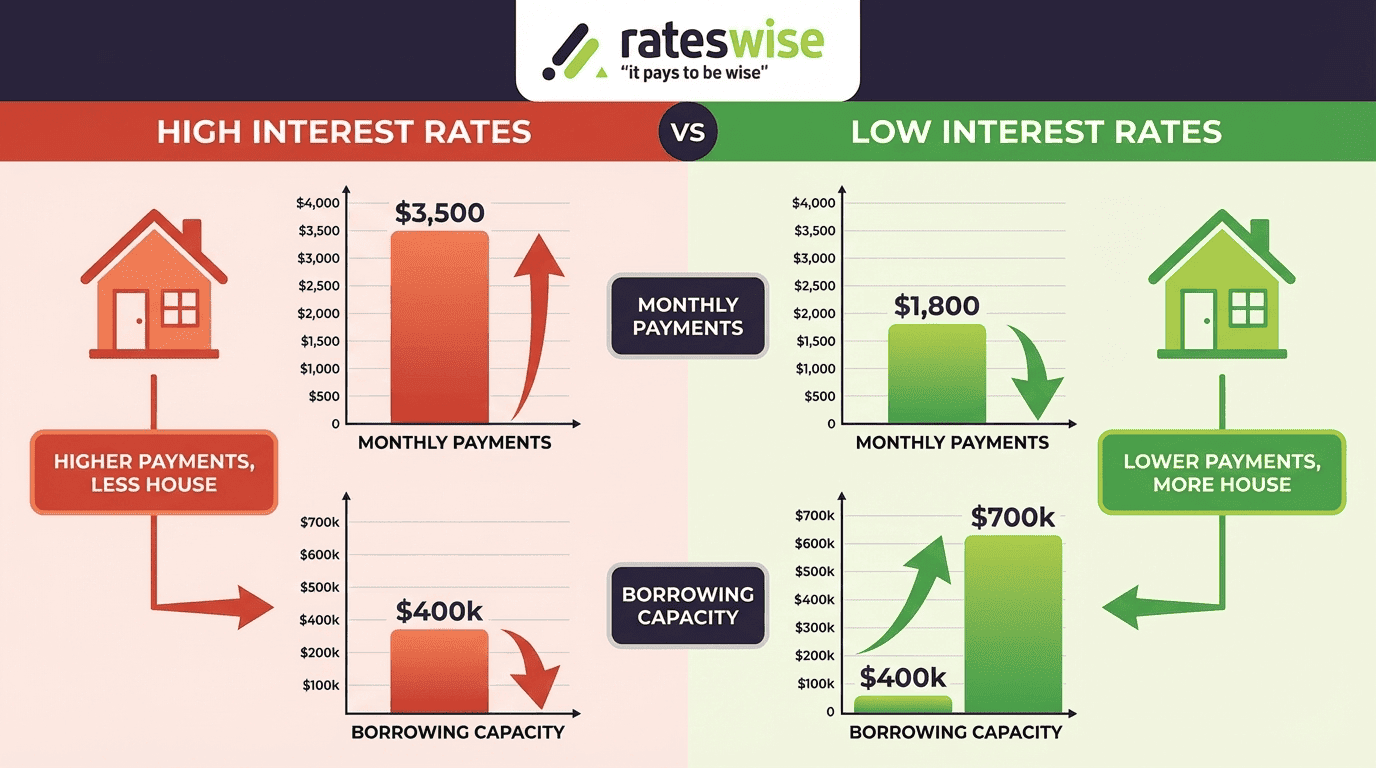

Interest rates have a direct impact on how much home you can borrow.

When rates increase:

- Monthly payments rise

- Borrowing capacity decreases

- Qualification becomes stricter

When rates decrease:

- Monthly payments become more manageable

- Borrowing capacity increases

Even small rate changes can significantly affect affordability.

Key Ratios Lenders Use to Calculate Affordability

Lenders rely on two core financial ratios:

Gross Debt Service Ratio (GDS)

The percentage of your income used for housing:

- Mortgage payments

- Property taxes

- Heating costs

A typical benchmark is up to 39%.

Total Debt Service Ratio (TDS)

The percentage of income used for all debt:

- Housing costs

- Credit cards

- Car loans

- Personal loans

The common threshold is up to 44%.

What is the affordability rule?

A basic way to estimate:

- Housing costs ≤ 39% of income

- Total debt ≤ 44%

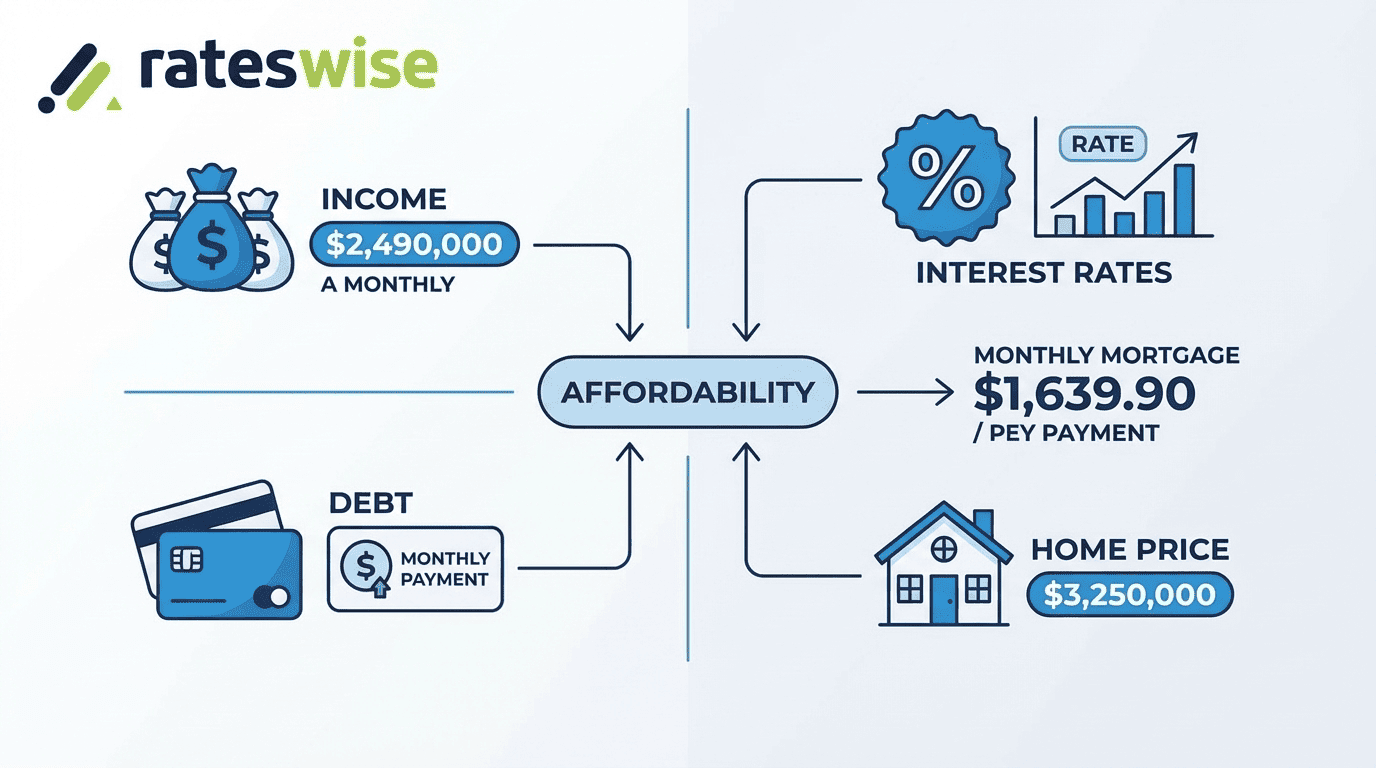

Example: Monthly income = $6,000

- Max housing = ~$2,340

- Max total debt = ~$2,640

This is a guideline, not a final approval.

Why You Should Not Borrow the Maximum

Just because you qualify for a certain mortgage amount does not mean you should borrow the maximum.

A more balanced approach considers:

- lifestyle expenses

- future financial goals

- job stability

- potential interest rate changes

A sustainable mortgage supports your life, not restricts it.

How Does Your Down Payment Affect Mortgage Affordability?

Your down payment directly influences how much home you need to borrow.

When you make a higher upfront investment, which lowers monthly payments and increases your overall financial flexibility.

In reality, this leads to:

- Reduce your monthly mortgage

- Better approval chances

- Lower interest over time

In Canada:

- Minimum starts at 5%

- Less than 20% requires insurance

A larger down payment improves flexibility.

Mortgage insurance is usually necessary if your down payment is less than 20%. This raises your overall expenses, but it may also enable you to join the market sooner.

What Price Range Can You Realistically Afford?

Instead of focusing only on lender approval, it is more useful to think in terms of a comfortable price range.

A simplified way to estimate this is:

- Start with your household income

- Apply debt ratios (GDS and TDS)

- Adjust based on your existing obligations

- Factor in your down payment

For example:

- A household with a stable income and minimal debt can allocate more toward housing

- A household with variable income or existing loans should stay conservative

The key is to align your purchase with long-term sustainability rather than short-term approval.

Real-World Affordability Example

Consider two buyers with similar income levels.

Buyer A

- no existing debt

- stable employment

- strong savings

This buyer can comfortably handle higher monthly payments and may qualify for a larger mortgage.

Buyer B

- Ongoing car payments

- credit card balances

- limited savings

Even with the same income, this buyer’s affordability is lower because their total financial obligations are higher.

👉 Insight: Affordability is not determined by income alone. It is defined by your financial profile.

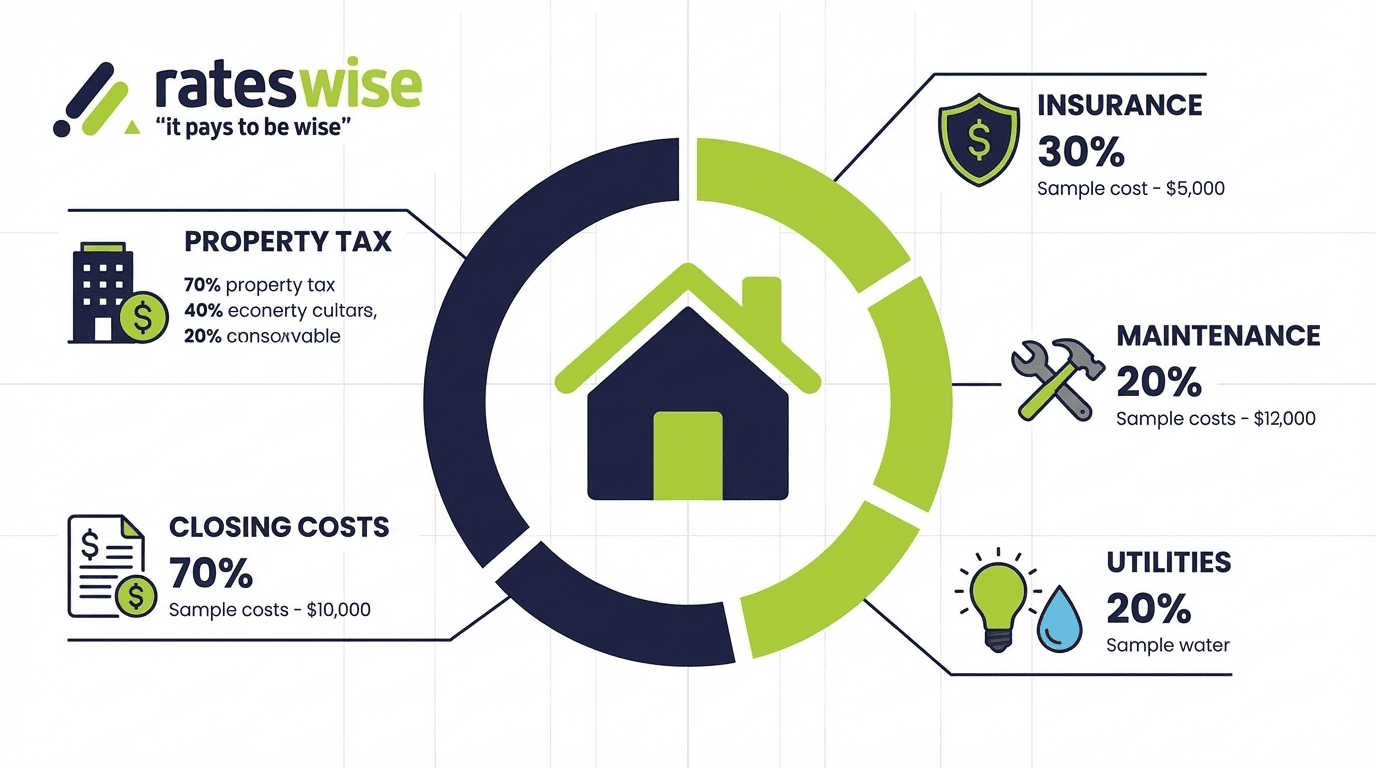

What Costs Should You Include Beyond Your Mortgage?

Many buyers underestimate the total cost of homeownership. Mortgage payments are only one part of the equation.

You also need to consider:

- Property taxes

- Insurance

- Maintenance and repairs

- Utilities

- Closing costs

Ignoring these leads to unrealistic budgeting.

Why Should Closing Costs Not Be Ignored?

Closing costs are an upfront expense and they typically include:

- Legal fees

- Land transfer taxes

- Inspection costs

- Lender-related charges

These costs are often underestimated, yet they require immediate liquidity. Buyers who do not plan for them may face financial strain even before moving in.

The Importance of Financial Buffer

Affordability should include a safety margin.

Unexpected situations such as:

- job changes

- rate increases

- emergency expenses

can impact your ability to maintain payments.

A well-planned mortgage decision includes:

- emergency savings

- manageable monthly obligations

- flexibility in spending

Approval Vs Sustainability

There is a clear difference between what a lender approves and what is financially sustainable.

Approval is lender's calculation.

Sustainability is real-life affordability.

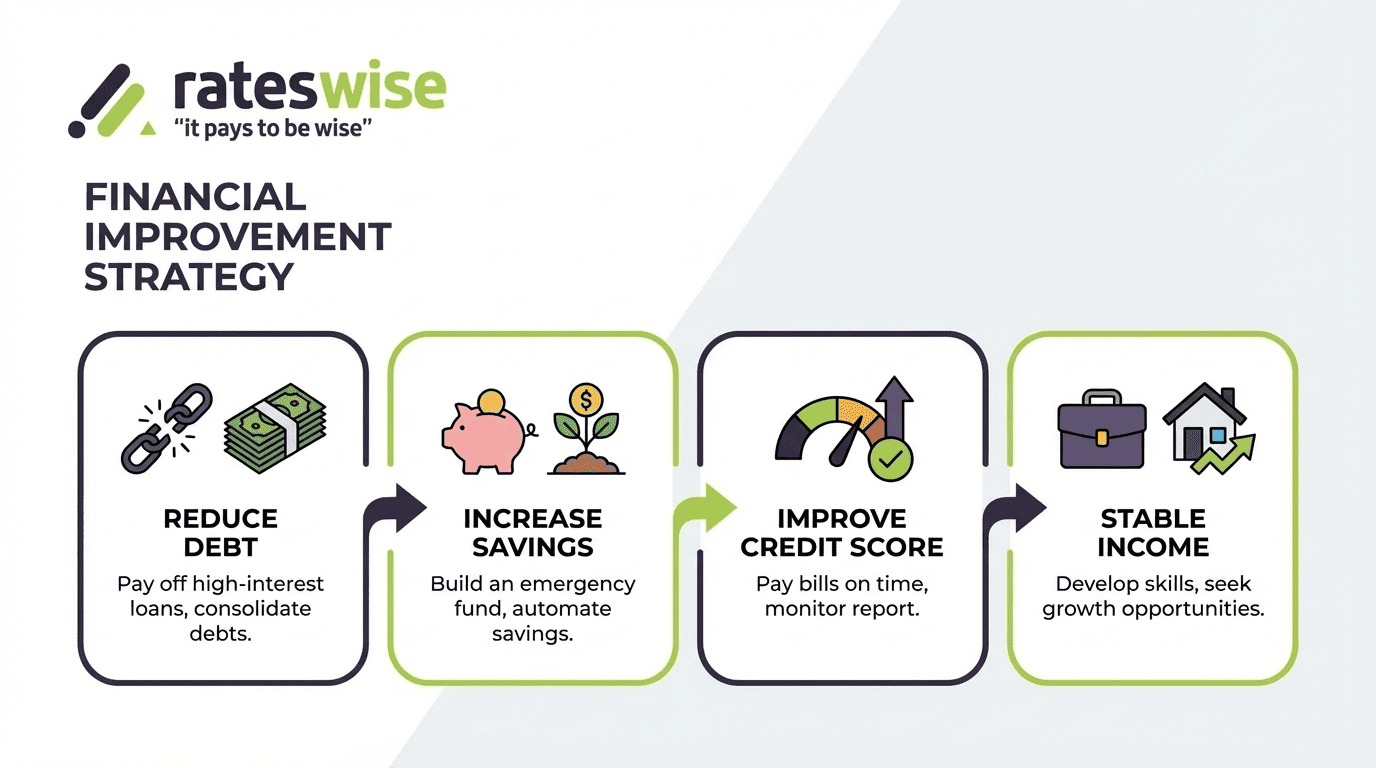

How Can You Improve Your Mortgage Affordability?

You can improve your mortgage affordability by strengthening three key areas: income stability, debt management, and financial preparation. Small adjustments in these areas can significantly increase your borrowing capacity and reduce financial pressure after purchase.

Affordability is not fixed. It can be improved with deliberate planning before applying for a mortgage.

Reduce Existing Debt

One of the most effective ways to improve affordability is to reduce your existing liabilities.

Lenders assess your total debt obligations when calculating how much you can borrow. Lower debt levels improve your financial profile and increase your eligibility.

Key steps include:

- Paying down with credit cards

- Avoid new personal loans

- Lower monthly obligations

Even a modest reduction in monthly obligations can have a meaningful impact on your borrowing capacity.

Increase Your Down Payment

A larger down payment does more than reduce your loan amount. It improves your overall financial positioning.

Benefits include:

- lower monthly payments

- reduced interest costs over time

- stronger application profile

For many buyers, strong savings can lead to better long-term affordability than rushing into a purchase.

Improve Your Credit Profile

Your credit score plays a role in determining the interest rate you receive. A stronger credit profile often results in more favorable terms.

Steps to improve your credit position:

- Make payments on time

- Keep credit utilization low

- Avoid frequent credit applications

A better interest rate directly improves affordability by lowering monthly payments.

Stabilize Your Income

Lenders value consistency and predictability.

Clear documentation also matters.

Stable income sources are viewed more favorably than irregular or fluctuating earnings. If your income varies, providing clear documentation becomes essential.

For example:

- Salaried employment is easier to assess

- Self-employed income requires detailed financial records

Improving income clarity can strengthen your application even if your earnings remain the same.

Choose the Right Mortgage Structure

Factors to consider:

- Fixed vs variable rates

- Amortization period

- Payment frequency

A longer amortization period reduces monthly payments but increases total interest over time. A shorter period does the opposite.

👉 Structure impacts affordability as much as income.

Common Mistakes That Reduce Affordability

Even financially stable buyers can make decisions that limit their borrowing potential.

Taking on New Debt Before Approval

Financing a vehicle or increasing credit balances before applying can reduce your eligibility.

Ignoring Total Monthly Costs

Focusing solely on mortgage payments without considering the full cost of ownership leads to unrealistic expectations.

Overestimating Future Income

Basing affordability on expected raises or future earnings can create financial pressure if those changes do not materialize.

Poor Documentation

Incomplete or inconsistent documentation can delay approval or weaken your application.

A Simple Decision Framework

To evaluate your readiness, ask:

- Are my monthly obligations manageable with room for flexibility?

- Do I have sufficient savings after the purchase?

- Can I handle a potential increase in interest rates?

- Am I buying within a comfortable range, not just the maximum approved?

If the answer to any of these is uncertain, it may be worth reassessing your budget before proceeding.

👉 Insight: Improving affordability is less about earning more and more about managing your financial structure effectively.

What Should You Expect From Mortgage Affordability in the Future?

Mortgage affordability depends on:

interest rates, inflation, and housing supply.

In general:

- Rising interest rates reduce affordability

- Stable or declining rates improve it

For buyers, this means affordability is not static. It changes over time.

How Interest Rate Trends Impact Buyers

One of the most crucial factors is still interest rates.

When rates go up, lenders use stress testing to make it harder for people to qualify. This limits the amount that buyers can borrow, even if their income remains constant.

Conversely, as rates fall or stabilize:

- Payments each month become more predictable.

- Buyer confidence rises as borrowing capacity improves

👉 Insight: Even small rate changes can significantly affect affordability over the life of a mortgage.

Market Behavior and Affordability Pressure

Housing demand and supply dynamics also influence affordability.

In markets with limited inventory:

- Prices tend to remain high

- Competition increases

- Buyers may feel pressure to stretch budgets

In more balanced conditions:

- Pricing becomes more stable

- Buyers have more negotiating power

- Affordability improves gradually

Understanding market conditions helps buyers avoid overcommitting financially.

ROI and Risk Overview

You should think about more than just how much a mortgage would cost you when making a decision. You should also think about how it will affect your finances in the long run.

Possible Benefits:

A well-planned mortgage selection can give you:

- Expansion of assets over time

- Costs of owning a home that are easy to anticipate

- Financial stability through regular payments

Key Risks to Consider

At the same time, customers should know about the risks:

- higher interest rates making payments more difficult

- unplanned costs that change monthly budgeting

- overleveraging based on the highest boundaries of approval

👉 The goal is not merely to get a mortgage, but to stay financially stable while you have it.

In the End

There isn't just one number that tells you how much you can afford to pay on your mortgage. It is a balance between money coming in, money going out, being responsible with money, and planning for the future.

A sustainable approach is based on:

- realistic budgeting

- monthly payments that are easy to handle

- keeping your finances flexible

Not just lender approvals, but also decisions about mortgages that fit with your lifestyle and future aspirations are the best ones.

Frequently Asked Questions

How much income do I need to afford a mortgage?

The required income depends on your financial obligations, down payment, and current interest rates. Lenders typically use debt ratios to determine eligibility.

What is considered an affordable mortgage payment?

A payment that fits your budget while leaving room for savings and expenses.

Does a higher down payment always improve affordability?

Yes. It reduces your loan and monthly payments.

Can I still qualify with existing debt?

Yes, but your borrowing capacity will be lower because lenders include all debt obligations in their calculations.

Should I borrow the maximum amount I am approved for?

Not necessarily. It is often better to stay below the maximum approval to maintain financial comfort and reduce risk.