First-Time Homebuyer’s Guide: Everything You Need to Know Before Buying

Do you want to buy a house in Canada? You are not on your own. Newcomers buy around one out of every five properties in Canada.

So, how do newcomers/first-home buyers buy a home in Canada?

Purchasing your first house may be fun and frustrating, particularly if you've no idea where to start. Thus, learn as much as you can about everything in purchasing real estate in Canada.

In this article, we’ll discuss the process involved in buying your first home and how to choose the perfect location and house of your dreams.

What defines a first-time home buyer?

A first-time home buyer is defined as someone who has never owned a home or never purchased a primary residence.

First-time homebuyers are eligible for exclusive offers such as lower down payments and closing cost help. Some lenders offer special loans and incentives.

Who Qualifies as a First-Time Homebuyer?

The term first-time home buyer can be confusing or misleading because, you may be eligible for various programs as a first-time home buyer, if you haven’t owned a home, or haven’t bought a house in the last three years.

Also, you can qualify to buy a property for the first time if you:

Are you a single parent or stay-at-home who, during the previous three years, co-owned a marital residence with your spouse

Or

Have not owned any investment or second property either alone or in partnership, nor have they owned a marital home.

Other First-Time Homebuyer Qualifications

To be eligible for many first-time home buyer programs, you must also meet other requirements rather than just a three-year requirement. Some of these requirements are:

- A credit score of at least 620. But 640 or 680 are needed for some programs.

- Debt-to-income (DTI) ratio of 43% or less

- A down payment contribution that varies based on the lending program

- A purchasing price and an income that is within program requirements

- Purchasing a house in a particular state, county, or city

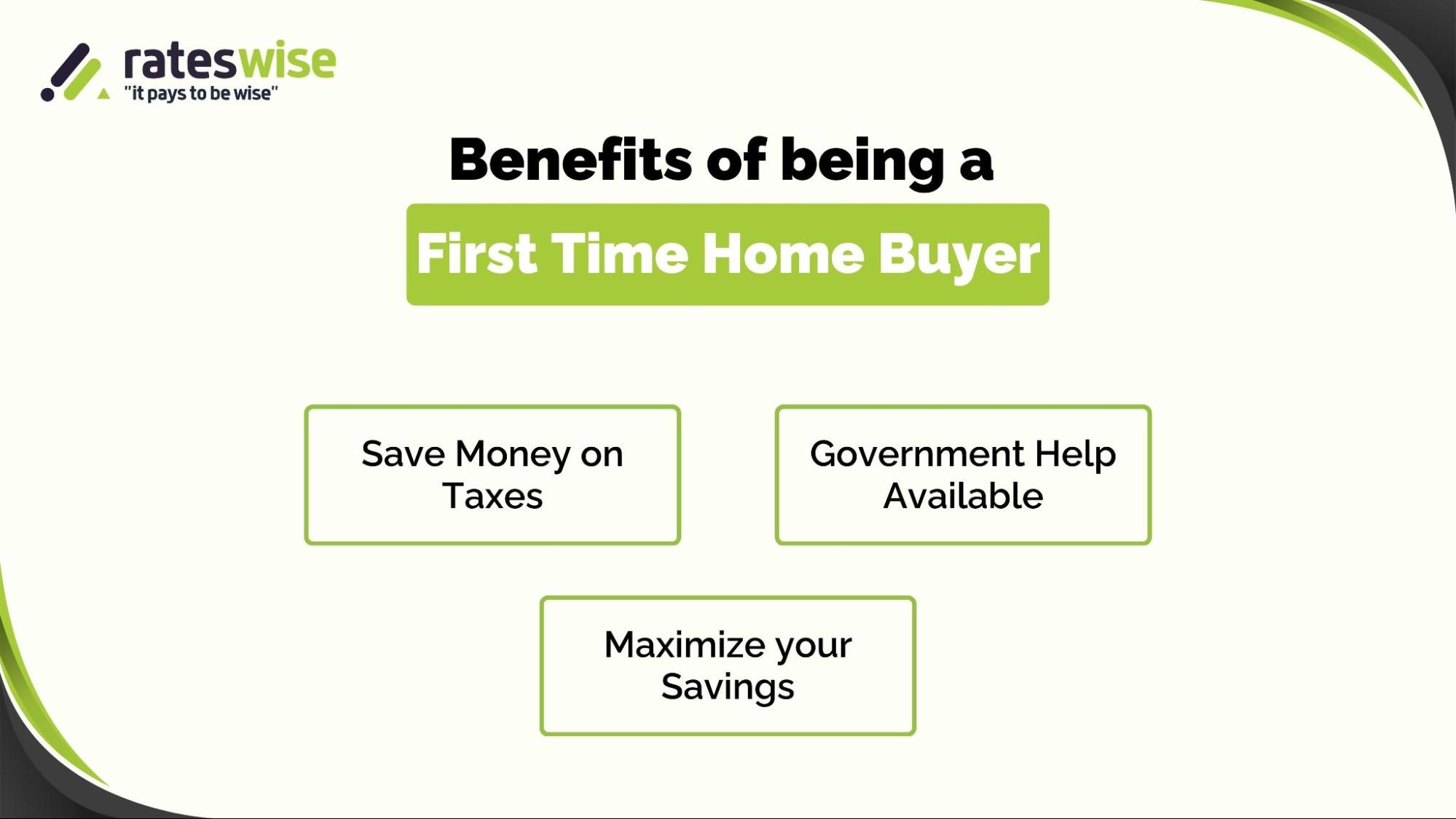

What Are the Benefits of Being a First-Time Buyer?

There are several advantages available to you if you are eligible for a first-time homebuyer loan or an assistance program, including:

Lower monthly installments:

Mostly first-time home buyer loans offer low interest rates, and in case PMI is needed, the cost is reduced or eliminated. Lowering these costs lowers your monthly payments, and makes it affordable for you.

Reduced down payments:

Certain programs allow third-party or down payment assistance. You can also get funds to cover closing costs.

Certificates of mortgage credit (MCCs):

You could save money on your taxes if you qualify for an MCC, which offers a dollar-for-dollar federal tax credit up to $2,000 annually.

Consider these things to make the best choice

- What are your long-term objectives?

- Next, think about how those plans align with home ownership.

- Some people want to convert all of those "wasted" rent payments into mortgage payments so they can acquire equity, a real asset. Some people like the concept of being their own landlord and take homeownership as a sign of their independence.

- Next is the question of whether purchasing a property is a wise investment.

- You'll be on the right track if you focus on your long-term homeownership goals.

You should ask yourself these questions whether you qualify as a first-time home buyer and what advantages you’ll get:

Here’s the list of some of those questions:

The first question: What can you afford?

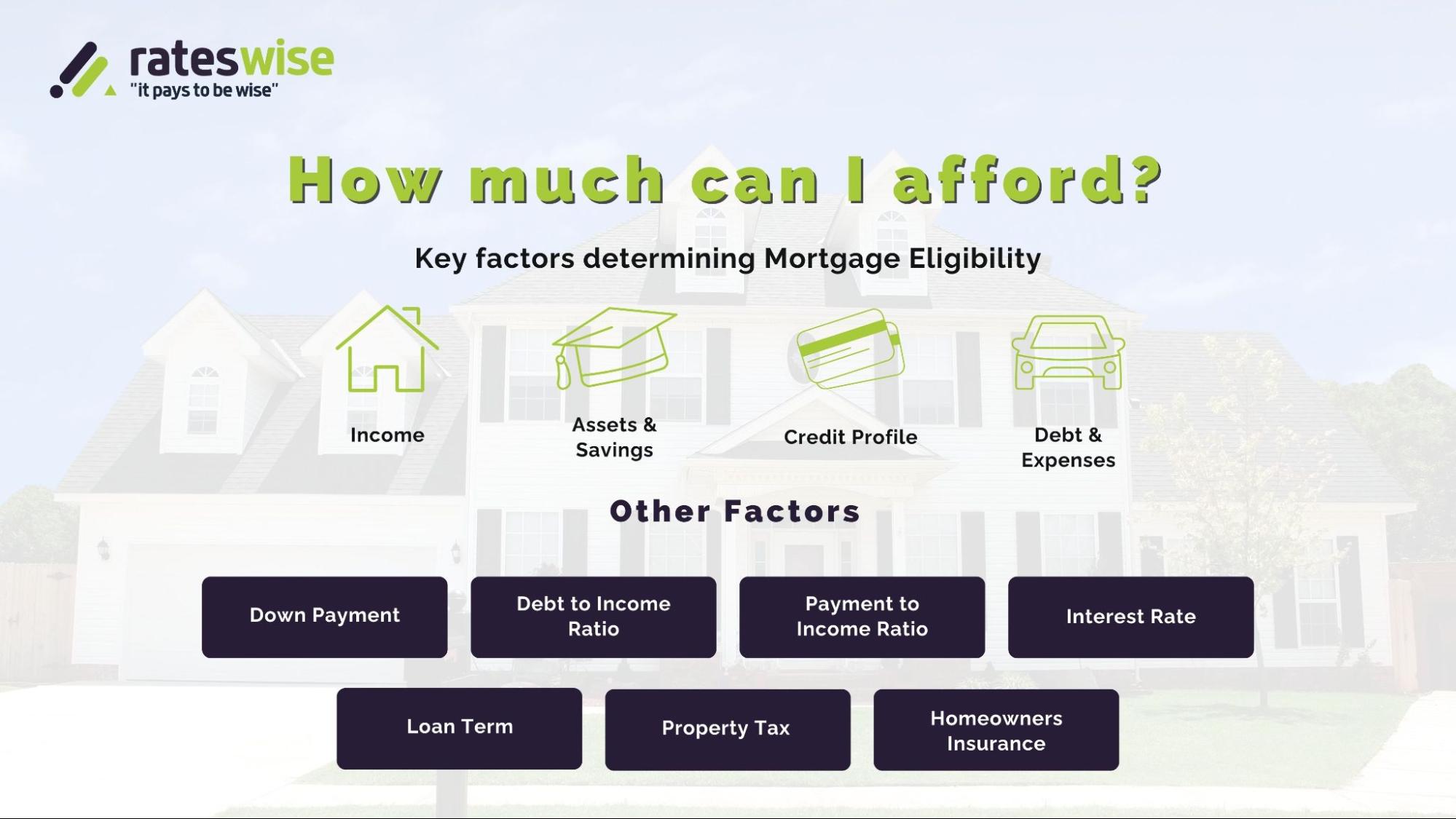

Consider your financial situation. The minimum down payment in Canada ranges from 5% to 20% of the purchasing price. You need to get mortgage default insurance if your down payment is less than 20%. A 20% down payment is required for homes over $1 million.

Set aside money for closing costs, property insurance, land transfer taxes, and property taxes. Find out how much you can afford by speaking with a mortgage specialist.

How can you save for a down payment?

Although it can be difficult, there are ways to save for a house. An RRSP increases your chance to buy your first home.

As long as you pay it back within 15 years, you can take out up to $35,000 ($70,000 for couples) tax-free as a down payment under Canada's First-Time Home Buyer's Plan.

Which type of house is more appropriate for you?

Once you have set your long-term goals, you can choose from a variety of residential property options, including townhouses, condominiums, single-family or multifamily homes, cooperatives, etc. Each option has its pros and cons, it depends on your goals.

What particular features would you like to see in your ideal home?

You deserve to put your heart and money into something that closely satisfies your requirements and desires because you're making the largest buy of your life. Make a list for that; it should cover anything from the most fundamental preferences, like neighborhood, to more specific ones, such as kitchen and bathroom layouts. Do your research and make the right decision that best suits your demands.

Know your mortgage eligibility

Lenders will decide how much they are willing to lend you.

For example:

Despite your belief that you can afford a $300,000 apartment, lenders might only consider you suitable for a $200,000.

Well the lender decides this by looking into certain factors such as:

- How much debt do you have

- Your monthly income

- Your current job’s duration

Many agents require mortgage pre-approval, and sellers frequently won't entertain offers without it. Verify your income and debt by researching lenders, comparing rates, and applying with the required paperwork.

Do you have enough savings?

If you want to buy a home, you need to pay a down payment of 3.5% to 20% with the closing charges. So you must consider Certificate of Deposit CDs if you want to purchase within the next three years, they offer growth while protecting your funds. A high-yield savings account is a better choice if you plan to make purchases within six to twelve months because it keeps your money safe and accessible.

Who will guide you through the home-buying process?

Finding homes, arranging visits, and managing paperwork are all assisted by a real estate agent. They also help with financing discussions, offers, and purchases. Their expertise can help them avoid expensive costs and the seller typically pays their commission.

What is the 20% rule for home purchases?

It is advised to make a 20% down payment in order to avoid mortgage insurance, obtain reduced interest rates, and increase equity growth. But if necessary, some lenders may accept smaller down payments.

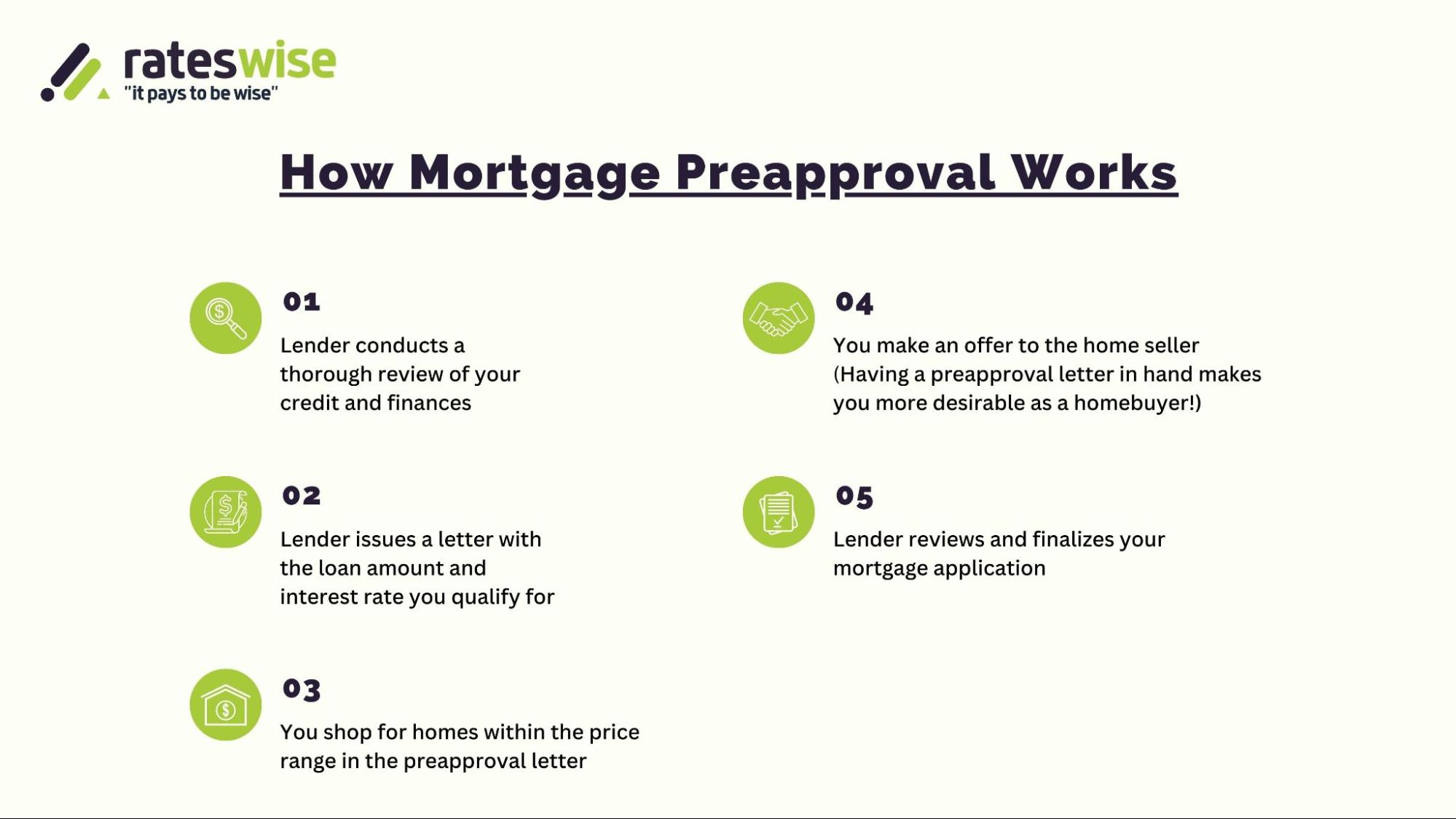

The Mortgage Pre-Approval Process in Canada

You may have to go through a mortgage pre-approval process before you purchase a home. Based on your financial situation, this helps you determine how much a lender will provide. Pre-approval is not necessary, however, it facilitates budgeting, offers, simplifies, and speeds up the mortgage process. It lasts between 60 and 120 days.

Buying Process

1- Find a Home

Use all available choices including online listings, real estate agents, and even word of mouth. Look at houses with potential if you're on a tight budget, even if they require only minimal renovations. First-time buyers must consider properties with potential that gain value over time.

2- Safe and Secure Funding

A low debt-to-income ratio, a history of on-time payments, and good credit these things impact your eligibility for a loan. Lenders say that housing expenses should not exceed 28 percent of your income.

Avoid significant financial changes (such as purchasing a car) because your loan isn't guaranteed until closing, even if you are pre-approved.

Find the best terms and rates by comparing lenders, and think about having a backup lender.

3- Make an Offer

Make an offer price and terms (such as the seller paying closing expenses) in consultation with your agent. Negotiate until both parties are satisfied.

Once you make an offer, make sure you save for extra costs such as utility bills, taxes, and closing fees, to avoid any surprises in the future.

After a deal is closed, you will enter escrow (usually for 30 days) and pay a good deposit.

4- Request a Home Inspection

When you visit and inspect personally, this will help you find any hidden problems, even if the house appears to be in ideal condition. If there are significant issues, you can request repairs, renegotiate, or request a refund.

5- Close the Deal

It is now time to sign the last documents if everything is in order. If your down payment is less than 20%, you need to prepare an appraisal, title check, and mortgage insurance before closing. Once it's completed, the house is yours.

Final Thoughts

Buying a home is a big decision, but learning about the process in advance can make it much easier. You must know these things such as mortgage pre-approval, funding options, and closing costs.

The more you educate yourself, then finding a property that suits your needs and budget will be easier and less stressful. Take your time, ask questions, trust the process, and make the right decision.

Disclaimer: This content is based on current facts and intended purely for informational purposes. Always ask your lender about current details.

Related Articles